Editorial Note: We are an inventory management software provider. While some of our blog posts may highlight features of our own product, we strive to provide unbiased and informative content that benefits all readers.

ABC analysis is a method used in inventory management to categorize stock items into three classes based on their relative importance. This helps organizations prioritize their efforts to manage inventory and reduce costs.

Class A items are the most important and valuable items in the inventory, representing a small percentage of the total inventory but accounting for the majority of its value. Class B items are less important but still contribute to the value of the inventory, while Class C items are the least important items with a low value relative to the total inventory.

The purpose of ABC analysis is to allow companies to focus their efforts and resources on the most valuable items, while still managing the rest of the inventory efficiently. It helps organizations to optimize their inventory management processes and make better use of their resources, reducing the risk of stock shortages and overstocking.

Pareto Principle & ABC Classifications:

The Pareto Principle, named after the Italian economist Vilfredo Pareto, was first introduced in the late 19th century. Pareto observed that approximately 80% of the land in Italy was owned by 20% of the population. He later expanded this observation to other areas of economics, including the distribution of wealth and income.

Pareto noticed that this 80/20 distribution was present in many other areas of life and coined the term “Pareto principle” to describe it. Over time, the principle has been applied to various fields, such as project management, quality control, and marketing, where it can be used to identify and prioritize the most important factors that contribute to a particular outcome.

For example, in business, the Pareto Principle suggests that 80% of a company’s sales may come from 20% of its customers, or that 80% of a company’s profits may come from 20% of its products. By applying this principle, companies can prioritize their efforts and allocate resources to the most impactful areas.

Purpose of Using ABC Analysis in Inventory Management:

The purpose of using ABC analysis in inventory management is to prioritize and allocate resources effectively by focusing on the most critical items in inventory. By categorizing items into “A”, “B”, and “C” groups, inventory management efforts can be tailored to meet the specific needs of each item, ensuring that resources and efforts are used efficiently and effectively.

ABC analysis helps to achieve the following key objectives in inventory management:

1. Maximize return on investment:

By focusing on “A” items, which typically represent the majority of the value of inventory, inventory management efforts can be focused where they will have the greatest impact.

2. Minimize inventory costs:

By prioritizing “C” items, which typically represent a small portion of the value of inventory, inventory management efforts can be minimized, reducing costs and increasing efficiency.

3. Balance inventory availability and cost:

By managing “B” items, inventory management efforts can be balanced between ensuring inventory availability and minimizing inventory costs.

4. Improve decision-making:

ABC analysis provides a clear and structured approach to inventory management, which helps to improve decision-making and ensure that resources are allocated effectively.

5. Enhance control:

By implementing reorder points and monitoring inventory levels, ABC analysis helps to ensure that inventory is available when needed, reducing the risk of stockouts and lost sales.

Understanding the ABC Classification:

Class A items typically have high demand, high unit value, and low inventory turnover. Class B items have moderate demand, moderate unit value, and moderate inventory turnover. Class C items have low demand, low unit value, and high inventory turnover.

1. “A” items:

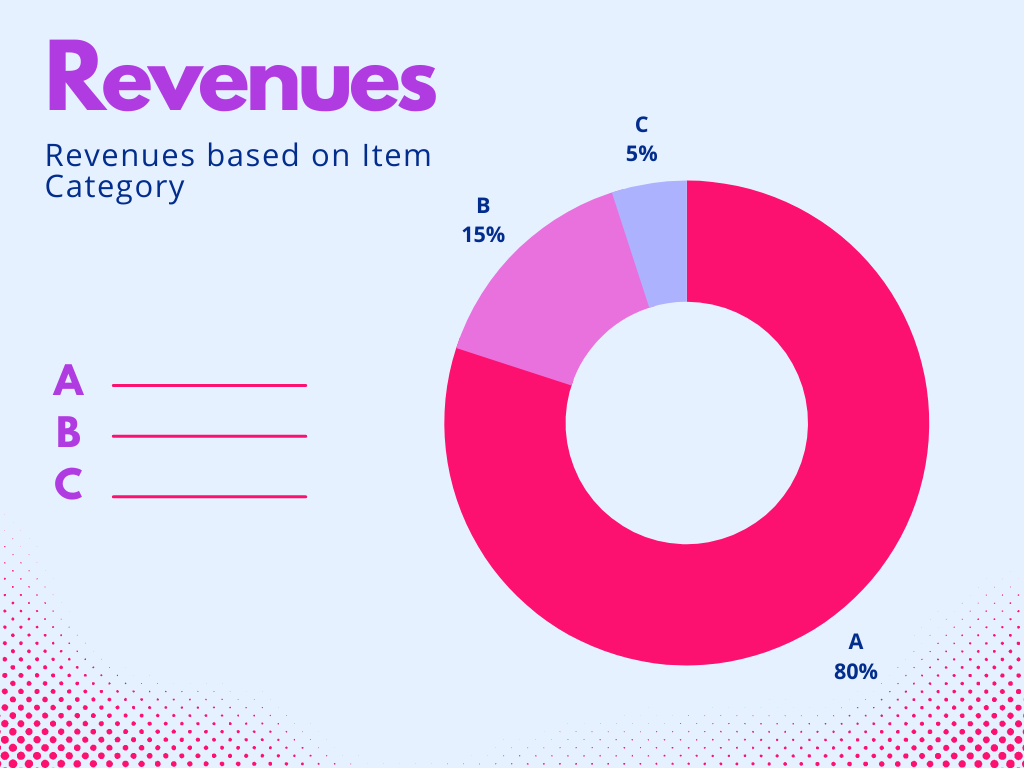

Category A items refer to the most important items in inventory management, typically representing the top 20% of inventory items that account for 80% of the total inventory value or sales. These items are considered the most critical to the success of a business and require the most frequent and detailed attention.

In ABC analysis, “A” items are given the highest priority for inventory management efforts, which typically includes frequent monitoring, careful planning, and strict control of inventory levels. This may involve implementing reorder points, setting up automated reordering systems, or even dedicating specific personnel to manage these items.

The goal of prioritizing “A” items is to ensure that they are always in stock and readily available to meet customer demand. This helps to minimize the risk of stockouts and lost sales, while also maximizing the return on investment in inventory management efforts.

2. “B” items:

Category B items refer to items of medium importance in inventory management, typically representing the next 30% of inventory items that account for around 15% of the total inventory value or sales. These items are considered less critical to the success of a business compared to “A” items but still require some attention and management.

In ABC analysis, “B” items are given a lower priority compared to “A” items, but still require some level of monitoring and control. This may involve implementing reorder points and minimum stock levels, and conducting regular reviews of inventory levels to ensure that they are adequate.

The goal of managing “B” items is to ensure that they are available when needed but without incurring excessive inventory costs. This helps to balance the need for inventory availability with the need to minimize inventory costs.

3. “C” items:

Category C items refer to the least important items in inventory management, typically representing the remaining 50% of inventory items that account for only 5% of the total inventory value or sales. These items are considered the least critical to the success of a business and require the least attention and management.

In ABC analysis, “C” items are given the lowest priority for inventory management efforts, which typically involves minimal monitoring and control. This may involve setting up a basic reordering system or simply monitoring inventory levels periodically.

The goal of managing “C” items is to minimize the amount of resources and effort dedicated to these items, while still ensuring that they are available when needed. This helps to minimize inventory costs while ensuring that inventory is still available when needed.

Benefits of ABC Analysis:

ABC analysis is a valuable tool for companies looking to improve their inventory management and drive better business results. It allows companies to prioritize their efforts by focusing on the most important items and allocating resources accordingly. Benefits of ABC analysis include improved inventory control and accuracy, reduced inventory holding costs, better risk management, improved forecasting, enhanced customer service, and improved reporting.

- Prioritization of efforts By focusing on the most valuable items, organizations can prioritize their efforts and resources on the items that matter the most, leading to improved inventory management and cost savings.

- Better resource allocation ABC analysis helps organizations allocate their resources more efficiently by directing their efforts towards the most valuable items, reducing the risk of stock shortages and overstocking.

- Reduction in stock shortages By focusing on Class A items, organizations can reduce the risk of stock shortages, ensuring that they always have sufficient stock to meet customer demand.

- Improved inventory management ABC analysis helps organizations to optimize their inventory levels, leading to improved efficiency and cost savings.

- Reduced costs by focusing on the most valuable items, organizations can reduce their inventory costs, freeing up resources that can be used for other purposes.

By using ABC analysis to manage inventory, companies can reduce waste, improve efficiency, and make better use of their resources, leading to improved overall performance and increased profitability.

How to Implement ABC Analysis:

implementing an ABC inventory management system can be a complex and time-consuming process, but it can lead to improved inventory management and cost savings. It is important to carefully consider the limitations of the method and to adjust the approach as needed to ensure that it is effective and appropriate for the organization’s specific needs.

Steps in implementing ABC analysis:

1. Collect Data:

The first step in implementing an ABC inventory management system is to collect data on inventory items. This should include information such as item costs, usage levels, lead times, and demand patterns.

2. Classify Inventory Items:

Once data has been collected, the next step is to classify items into A, B, and C categories based on their importance. This can be done using a variety of methods, such as using cost as the primary criterion or considering other factors such as lead time, demand variability, and criticality to operations.

3. Re-evaluating the analysis regularly

It is important to re-evaluate the ABC classification regularly to ensure that it remains relevant and accurate. This can be done on a yearly or semi-annual basis, depending on the needs of the organization.

Incorporating ABC analysis into the overall inventory management process ABC analysis should be integrated into the overall inventory management process, including the development of policies, procedures, and systems for managing inventory. This will help ensure that the benefits of ABC analysis are realized and that inventory management is optimized.

Challenges in Implementing ABC Analysis:

Resistance to change Change can be difficult for some organizations and employees, and the implementation of ABC analysis may be met with resistance. To overcome this challenge, it is important to clearly communicate the benefits of ABC analysis and involve employees in the implementation process.

1. Difficulty in determining item value

Determining the value of each item in the inventory can be challenging, particularly if the organization has a large number of items. To overcome this challenge, it is important to have accurate and up-to-date data and to use a systematic approach to calculating the value of each item.

2. Inaccurate data

The accuracy of the ABC analysis is dependent on the accuracy of the data used to determine the value of each item in the inventory. To overcome this challenge, it is important to have a reliable data management system and to regularly review and update the data.

3. Limited resources

Implementing ABC analysis can require significant resources, including personnel and software. To overcome this challenge, it is important to prioritize the implementation of ABC analysis and allocate resources accordingly.

Implementing ABC Inventory Management Using Software:

Implementing an ABC inventory management system using software can simplify and automate many of the steps involved in implementing an ABC inventory management system. It is important to choose a software solution that meets the specific needs of the organization and to integrate it with other systems to ensure effective and comprehensive inventory management.

Implementing an ABC inventory management system using software involves several steps, including the following:

1. Select Software:

Choose a suitable software solution that meets the needs of the organization. The software should be able to handle the data required for ABC analysis and provide the necessary reporting and analytics capabilities.

2. Data Collection:

Collect the necessary data on inventory items, including costs, usage levels, lead times, and demand patterns. This data should be entered into the software and updated regularly to ensure that it is accurate and up-to-date.

3. Classify Inventory Items:

Use the software to classify items into A, B, and C categories based on their importance. This can be done using a variety of methods, such as using cost as the primary criterion or considering other factors such as lead time, demand variability, and criticality to operations.

4. Monitoring and Review:

Use the software to monitor and review the implementation of the ABC inventory management system. The software should provide regular reports and analytics that help assess the effectiveness of the system and identify areas for improvement.

An Example:

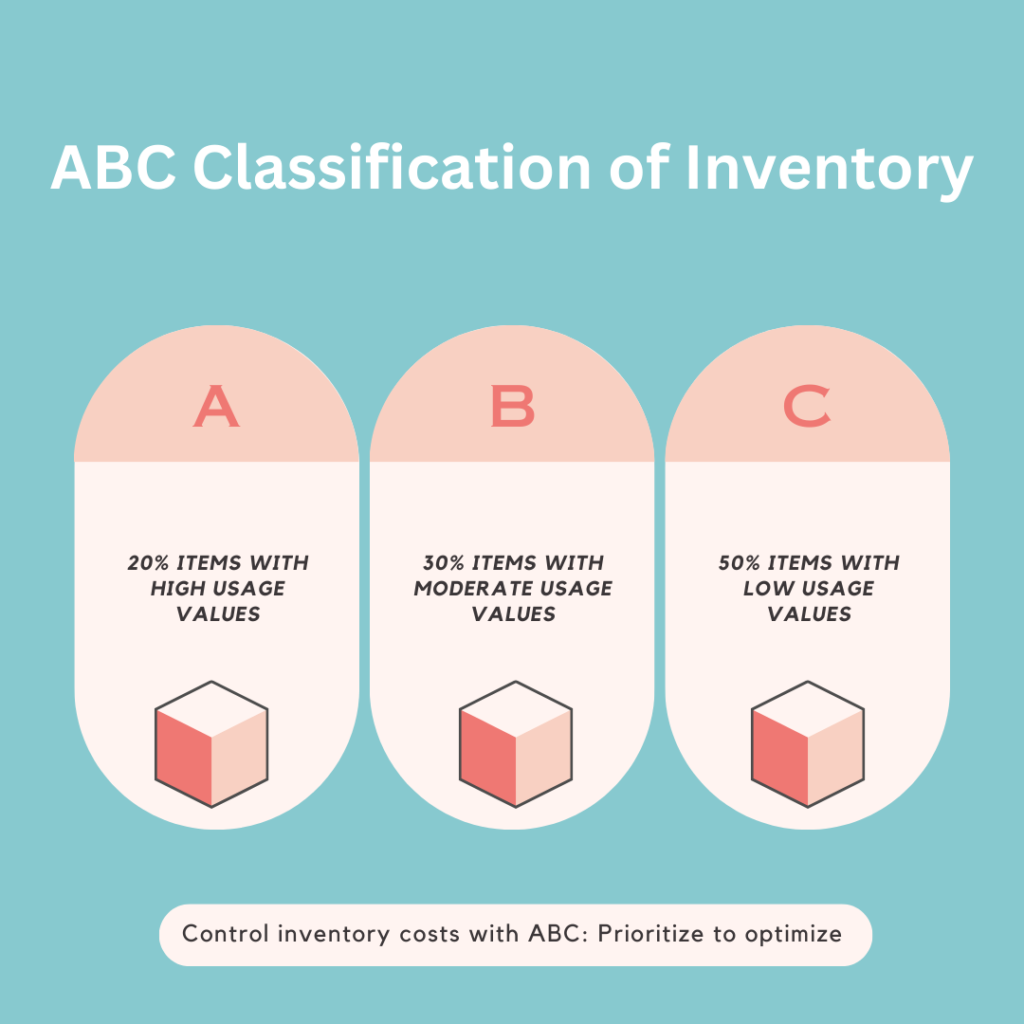

A business has 100 different inventory items. After conducting an ABC analysis, the manufacturer classifies the items as follows:

- A items: 20% items with high usage values.

- B items: 30% items with moderate usage values.

- C items: 50% items with low usage values.

The business then develops inventory management strategies for each category of items. For example, high-value A items may require frequent monitoring and tight control, while low-value C items may require less attention and can be managed with lower levels of safety stock. B items may require a balance between monitoring and control, and safety stock levels.

By applying ABC analysis, the business can focus its inventory management efforts on the most important items, while reducing the level of effort required for lower value items. This can help the business to optimize inventory management and minimize costs.

Limitations of ABC Analysis:

ABC analysis, also known as ABC classification, is a method used in inventory management to categorize inventory items based on their importance and prioritize the management of those items. However, there are several limitations to this method:

1. Limited Data Availability:

The accuracy of ABC analysis is dependent on the availability and accuracy of data, such as cost and usage information. If this data is not available or is inaccurate, the ABC classification may not accurately reflect the priority of items.

2. Doesn’t Consider Inter-Item Relationships:

ABC analysis doesn’t take into account the relationships between items and how changes to one item can affect the demand for other items. This can lead to incorrect categorization of items and misallocation of resources.

3. Not Suitable for All Business Types:

ABC analysis may not be suitable for all types of businesses, especially those with highly seasonal demand patterns or those that operate in highly dynamic markets.

Conclusion:

ABC analysis is an important tool for optimizing inventory management and reducing costs. By incorporating ABC analysis into the overall inventory management process, organizations can achieve significant benefits and improve their bottom line.

Related Post:

Safety Stock – Definition, Importance, Formulas & Implementation

There are a few different formulas that go into deciding how much safety stock you have to maintain. These include General formula,…

Click here to Read This Article

Take a Quiz Test - Test Your Skill

Test your inventory management knowledge. Short multiple-choice tests, you may evaluate your comprehension of Inventory Management.