Editorial Note: We are an inventory management software provider. While some of our blog posts may highlight features of our own product, we strive to provide unbiased and informative content that benefits all readers.

Inventory valuation refers to the process of assigning a monetary value to a company’s inventory or stock of goods for accounting and financial reporting purposes. The value of inventory is determined by considering the cost of acquiring or producing the goods, including any associated costs such as shipping, handling, and storage.

The valuation of inventory is an important component of a company’s financial statements, as it can impact the profitability, liquidity, and tax liability of the business.

Importance of Inventory Valuation for Businesses:

Inventory valuation is important for businesses for several reasons:

- Accurate financial reporting: Inventory valuation is a key component of a company’s financial statements, including the balance sheet and income statement. Accurate inventory valuation helps ensure that the financial statements are accurate and reliable, which is important for stakeholders such as investors, lenders, and regulators.

- Profitability analysis: Accurate inventory valuation is essential for calculating the cost of goods sold (COGS), which is a key component of calculating the gross profit margin. A higher COGS reduces the gross profit margin, which can impact a company’s profitability.

- Tax implications: Inventory valuation can impact a company’s tax liability. The method chosen for inventory valuation can impact the amount of taxes owed, as different methods can result in different COGS and net income figures.

- Budgeting and forecasting: Inventory valuation is important for budgeting and forecasting, as it helps businesses predict the amount of inventory needed and the cost of acquiring or producing that inventory.

- Inventory management: Accurate inventory valuation is essential for effective inventory management. It helps businesses identify slow-moving or obsolete inventory, as well as identify opportunities to optimize inventory levels to reduce costs and improve cash flow.

Inventory Valuation Methods:

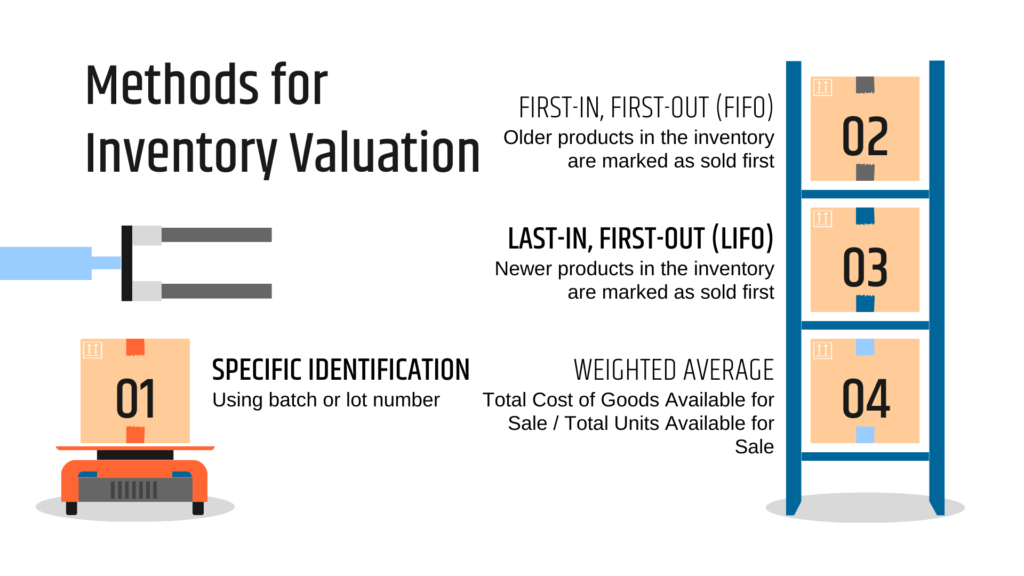

There are several inventory valuation methods that businesses can use to assign a value to their inventory. The most common inventory valuation methods are:

- First-In, First-Out (FIFO): This method assumes that the first items purchased are the first items sold, so the cost of goods sold (COGS) is based on the cost of the oldest inventory. The remaining inventory is valued at the cost of the most recent purchases. This method is often used in industries where the value of inventory tends to increase over time, such as the food industry.

- Last-In, First-Out (LIFO): This method assumes that the last items purchased are the first items sold, so the COGS is based on the cost of the most recent purchases. The remaining inventory is valued at the cost of the oldest inventory. This method is often used in industries where the value of inventory tends to decrease over time, such as the tech industry.

- Weighted Average Cost (WAC): This method calculates the average cost of all items in inventory, based on the total cost of all items divided by the total number of items. The COGS is then calculated based on the weighted average cost of the inventory sold. This method is often used in industries where the cost of inventory fluctuates significantly over time.

- Specific Identification: This method involves tracking the cost of each individual item in inventory, so the COGS is based on the specific cost of the items sold. This method is often used in industries where the cost of inventory is high and each item can be uniquely identified, such as the jewelry industry.

The choice of inventory valuation method can have a significant impact on a company’s financial statements and tax liability. Businesses should carefully consider their industry, inventory turnover, and financial reporting needs when selecting an inventory valuation method. Additionally, it is important to apply the chosen method consistently over time to ensure accurate reporting.

1. FIFO: First In, First Out

The first-in, first-out (FIFO) method is an inventory valuation method in which the cost of goods sold (COGS) is based on the cost of the oldest inventory items. The remaining inventory is valued at the cost of the most recent purchases. This method assumes that the first items purchased are the first items sold, which is why it is called the “first-in, first-out” method.

To calculate COGS using the FIFO method, the cost of the oldest inventory items is matched with the revenue from the first units sold. As new units are sold, the cost of those units is matched with revenue, until all inventory is sold. The value of the remaining inventory is based on the cost of the most recent purchases.

Imagine your store shelves like a queue. The FIFO (First In, First Out) inventory method operates exactly as it sounds: the first items acquired are the first ones sold. This method offers distinct advantages and disadvantages, making it suitable for specific business types and inventory compositions. Let’s explore its intricacies:

Advantages:

- Matches the physical flow of goods: FIFO aligns with how most businesses naturally operate, reducing confusion and simplifying inventory management.

- Accurate cost of goods sold (COGS) in stable or declining prices: During stable or declining pricing periods, FIFO accurately reflects COGS, leading to a clearer picture of profitability.

- Reduces risk of spoilage: For businesses like grocery stores, selling older items first minimizes the risk of expired inventory and potential losses.

- Compliance with international standards: FIFO adheres to International Financial Reporting Standards (IFRS), making it mandatory for businesses operating in certain regions.

Disadvantages:

- Overestimating COGS in inflation: When prices rise, FIFO overestimates COGS, potentially lowering reported profits and increasing tax burdens.

- Complex record-keeping for diverse inventory: Managing multiple purchase prices for different items can add complexity to record-keeping.

- Potential manipulation risks: Deliberately manipulating purchase dates can affect financial statements, although less so compared to other methods.

Suitable for:

- Businesses with stable or declining prices: Retailers, wholesalers, and manufacturers with consistent or decreasing pricing benefit from FIFO’s accurate COGS representation.

- Perishable goods: Grocery stores, pharmacies, and restaurants dealing with expiring items rely on FIFO to minimize spoilage and maximize freshness.

- Businesses complying with IFRS: Companies operating in regions requiring IFRS adherence must utilize FIFO for inventory valuation.

Think twice before using FIFO:

- Businesses with volatile pricing: Industries experiencing fluctuating prices might see their profitability distorted by FIFO, making LIFO or WAC more suitable options.

- Companies prioritizing tax minimization: LIFO generally offers tax advantages during inflation, whereas FIFO might increase tax burdens.

Remember: Choosing the right inventory valuation method depends on your specific business context. Consider industry norms, inventory composition, price trends, and tax implications before making a decision. Consulting with an accountant can ensure you select the method that best aligns with your strategic goals and regulatory requirements.

By understanding the nuances of FIFO, you can leverage its strengths while being mindful of its limitations, ultimately choosing the method that best drives your business forward.

2. LIFO: Last In, First Out

The last-in, first-out (LIFO) method is an inventory valuation method in which the cost of goods sold (COGS) is based on the cost of the most recent inventory items. The remaining inventory is valued at the cost of the oldest inventory items. This method assumes that the last items purchased are the first items sold, which is why it is called the “last-in, first-out” method.

To calculate COGS using the LIFO method, the cost of the most recent inventory items is matched with the revenue from the first units sold. As new units are sold, the cost of those units is matched with revenue, until all inventory is sold. The value of the remaining inventory is based on the cost of the oldest inventory items.

Imagine walking into a bakery where the newest, freshest cakes are always sold first. That’s essentially the LIFO (Last In, First Out) inventory method! Unlike FIFO, LIFO assumes the latest acquired items are sold first, leading to some unique advantages and disadvantages:

Advantages:

- Tax savings in inflationary periods: LIFO lowers reported profits by using more recent, higher purchase prices for COGS, potentially reducing tax liability.

- Better reflects current market costs: During inflation, LIFO’s COGS calculation aligns closer to current replacement costs, providing a more accurate picture of profitability.

- Reduces write-downs due to inflation: As older, lower-cost items remain in inventory, the risk of write-downs due to inflation diminishes.

- Improved cash flow: Lower reported profits translate to potentially lower tax payments, improving cash flow in the short term.

Disadvantages:

- Potential profit distortion in non-inflationary periods: When prices are stable or falling, LIFO can overestimate COGS, artificially lowering reported profits.

- Complex record-keeping: Tracking separate layers of inventory with varying costs can be complex and time-consuming.

- Less transparency than FIFO: Investors and analysts might find LIFO’s inventory valuation less transparent compared to FIFO.

- Not compliant with IFRS: International Financial Reporting Standards (IFRS) prohibit LIFO, limiting its use in certain regions.

Suitable for:

- Businesses with rising prices: Industries like manufacturing, oil & gas, and construction often experience fluctuating costs, making LIFO’s tax benefits appealing.

- Companies focused on short-term cash flow: LIFO’s potential tax savings can be advantageous for businesses prioritizing immediate cash flow management.

- Entities operating in non-IFRS regions: For companies outside jurisdictions requiring IFRS compliance, LIFO remains a viable option.

Think twice before using LIFO:

- Businesses with stable or declining prices: LIFO can distort profitability in such scenarios, making FIFO or WAC more suitable alternatives.

- Companies seeking long-term financial transparency: Investors and analysts might prefer the clarity offered by FIFO or WAC over LIFO’s layered cost structure.

- Entities operating in IFRS regions: Using LIFO would be non-compliant and lead to legal and reporting issues.

Remember: Selecting the right inventory valuation method requires careful consideration. Analyze your industry, pricing trends, tax implications, and long-term goals before choosing LIFO. Consulting with an accountant can ensure you navigate the complexities and choose the method that best serves your business needs.

By understanding LIFO’s unique characteristics, you can decide whether this “inflation warrior” aligns with your business strategy and helps you achieve your financial objectives.

3. WAC: Weighted Average Cost

The weighted average cost (WAC) method is an inventory valuation method in which the cost of goods sold (COGS) is based on the average cost of all inventory items. This method takes into account the cost of all inventory items purchased during a period, and calculates the average cost per unit of inventory.

To calculate COGS using the WAC method, the total cost of all inventory items is divided by the total number of inventory items to calculate the average cost per unit. This average cost is then multiplied by the number of units sold during the period to determine COGS. The value of the remaining inventory is based on the weighted average cost per unit of all inventory items.

Imagine blending different flavors of coffee beans to create a unique, consistent brew. That’s the essence of the Weighted Average Cost (WAC) method for inventory valuation! Instead of focusing on specific purchase dates like FIFO or LIFO, WAC considers the average cost of all similar items in stock, regardless of when they were acquired. Let’s explore its advantages, disadvantages, and suitability for different businesses:

Advantages:

- Simplicity and efficiency: Calculating WAC is typically easier than FIFO or LIFO, requiring less tracking of individual purchase prices.

- Flexibility for diverse inventory: WAC works well for businesses with numerous variations of the same product or frequent purchases at varying prices.

- Reduces record-keeping complexity: By using an average cost, WAC simplifies inventory management and record-keeping compared to methods like LIFO.

- Provides a general cost representation: WAC offers a broader picture of overall inventory cost, smoothing out fluctuations in individual purchase prices.

Disadvantages:

- Limited transparency in volatile markets: During significant price changes, WAC may not accurately reflect the actual cost of individual items sold.

- Less precise COGS calculation: Compared to FIFO/LIFO, WAC’s average cost might not exactly match the true COGS for specific inventory items.

- Potential masking of cost trends: By averaging costs, WAC can obscure underlying trends in purchase prices, making it harder to identify cost-saving opportunities.

- Not optimal for perishable goods: WAC doesn’t prioritize selling older items first, which might not be ideal for businesses managing perishable inventory.

Suitable for:

- Businesses with steady purchase prices: WAC shines when purchase costs remain relatively stable, avoiding significant distortions in COGS calculations.

- Companies with diverse inventory compositions: For businesses offering numerous variations of the same product or frequent purchases with varying prices, WAC simplifies cost management.

- Entities seeking simplified record-keeping: WAC’s efficiency can be advantageous for businesses prioritizing streamlined inventory management and reduced administrative burden.

Think twice before using WAC:

- Businesses with volatile pricing: If your industry experiences frequent price fluctuations, WAC’s averaged cost might not accurately reflect true COGS, potentially distorting profitability.

- Companies requiring precise COGS: If precise cost calculations are crucial for your business decisions, FIFO or LIFO might offer better accuracy than WAC’s blended approach.

- Entities needing to track cost trends: WAC can mask underlying cost variations, making it less suitable for businesses needing to identify and address cost-saving opportunities.

- Businesses managing perishable goods: For industries like food or pharmaceuticals, FIFO’s focus on selling older items first could be more appropriate than WAC’s averaged approach.

Remember: WAC is a valuable tool, but it’s not a one-size-fits-all solution. Analyzing your specific business needs, industry norms, inventory composition, and desired level of cost transparency is crucial before choosing WAC. Consulting with an accountant can help you weigh the pros and cons and select the inventory valuation method that best aligns with your strategic goals.

By understanding the nuances of WAC, you can leverage its efficiency and simplicity while being mindful of its limitations, ultimately choosing the method that helps you accurately manage your inventory costs and optimize your business performance.

4. Specific Identification:

The specific identification method is an inventory valuation method in which the cost of goods sold (COGS) is based on the actual cost of each individual inventory item sold. This method is used when businesses can specifically identify the cost of each inventory item sold, such as in the case of high-value or unique items.

To calculate COGS using the specific identification method, the cost of each individual inventory item sold is used to calculate the total cost of goods sold. The value of the remaining inventory is based on the cost of the unsold inventory items.

Imagine tracking every unique fingerprint in your inventory. That’s the essence of the Specific Identification Method! Unlike FIFO, LIFO, or WAC, this method meticulously tracks the individual cost of each item, offering distinct advantages and disadvantages:

Advantages:

- Pinpoint accuracy: You know the exact cost of each item sold, leading to the most precise COGS calculation and clearest picture of profitability.

- Enhanced financial reporting: Provides detailed information on inventory composition and valuation, improving the transparency and accuracy of financial statements.

- Better inventory management: By tracking specific costs, you can identify high-margin items, optimize pricing strategies, and make informed decisions about individual products.

- Tax benefits in specific scenarios: Depending on tax regulations, matching specific costs to specific sales can offer tax advantages in certain situations.

Disadvantages:

- Complexity and administrative burden: Requires meticulous tracking of purchase costs, serial numbers, or other unique identifiers for each item, increasing administrative demands.

- Limited scalability: Suitable for businesses with smaller, high-value, or easily identifiable inventory, scaling poorly for larger volumes or diverse product lines.

- Higher implementation costs: Setting up and maintaining a robust tracking system can be expensive compared to simpler methods like WAC.

- Potential manipulation risks: Deliberately mismatching costs to sales can occur, although robust tracking mitigates this risk.

Suitable for:

- Businesses with high-value or unique inventory: Ideal for jewelers, art galleries, car dealerships, or companies selling limited-edition items where individual costs matter.

- Entities requiring detailed financial reporting: Businesses with strict reporting requirements or needing precise inventory valuation benefit from the transparency offered.

- Companies prioritizing accurate cost management: When individual item costs significantly impact profitability, specific identification provides unmatched insight.

- Businesses in specific tax environments: Depending on tax regulations, precise cost tracking can offer tax advantages in some cases.

Think twice before using Specific Identification:

- Businesses with large, diverse inventory: Managing individual costs becomes impractical and inefficient for high-volume or varied product lines.

- Companies prioritizing administrative efficiency: The complexity and effort involved might outweigh the benefits for businesses aiming for streamlined operations.

- Entities with limited resources: Implementing and maintaining the tracking system can be costly, making it less suitable for businesses with budget constraints.

Remember: Specific Identification offers unparalleled accuracy but comes with complexity and cost considerations. Analyze your inventory composition, value, reporting needs, and budget before choosing this method. Consulting with an accountant can help you assess its suitability and navigate the implementation challenges.

By understanding the unique potential of Specific Identification, you can decide if its detailed tracking aligns with your business needs and helps you achieve precise inventory valuation and superior financial insights.

How Inventory Valuation Methods Impact Financial Statements and Taxes:

Choosing the right inventory valuation method isn’t just about numbers; it has a profound impact on your financial statements and tax implications. Understanding these connections is crucial for businesses to make informed decisions and optimize their financial health.

Impact on Financial Statements:

- Balance Sheet: Different methods affect ending inventory value, impacting total assets and shareholders’ equity.

- FIFO: Higher ending inventory values during inflation, boosting assets but potentially overestimating profitability.

- LIFO: Lower ending inventory values during inflation, reducing assets but potentially underestimating profitability.

- WAC: Averages out price fluctuations, leading to a moderate ending inventory value.

- Specific Identification: Precisely reflects individual item costs, showcasing the most accurate value on the balance sheet.

- Income Statement: COGS calculations vary with each method, influencing net income and profitability ratios.

- FIFO: Higher COGS in inflationary periods, potentially lowering reported profits.

- LIFO: Lower COGS in inflationary periods, potentially inflating reported profits.

- WAC: Smooths out cost fluctuations, offering a more stable but potentially less accurate COGS representation.

- Specific Identification: Matches exact costs to sold items, providing the most accurate COGS calculation but potentially increasing complexity.

Tax Implications:

- Taxable Income: The chosen method significantly influences reported taxable income, impacting tax liability.

- FIFO: Generally leads to higher taxable income in inflationary periods, resulting in potentially higher taxes.

- LIFO: Can lower taxable income in inflationary periods, offering potential tax savings.

- WAC: May fall between FIFO and LIFO in terms of tax implications, depending on specific circumstances.

- Specific Identification: Offers limited tax flexibility compared to other methods.

Additional Considerations:

- Industry Norms: Some industries have preferred methods (e.g., LIFO common in manufacturing).

- Financial Reporting Goals: Transparency and accuracy desired in financial statements should be considered.

- Company Strategy: Short-term tax benefits vs. long-term financial transparency need to be balanced.

Remember: Consult with your accountant to carefully evaluate the impact of each method on your unique business context and choose the one that best aligns with your strategic goals and regulatory requirements. By understanding the interplay between inventory valuation, financial statements, and tax implications, you can make informed decisions that optimize your business performance and financial position.

Inventory Valuation Methods in Diverse Economic Climates:

While FIFO, LIFO, WAC, and Specific Identification offer basic inventory valuation mechanisms, their true significance unfolds when examined through the lens of different economic climates and real-world business decisions. Let’s delve deeper into their nuances:

Inflationary Environments:

- FIFO: Higher COGS during inflation translates to lower net income, potentially impacting dividend payouts and investor confidence. However, it aligns with physical flow in certain industries and simplifies tax accounting.

- LIFO: Lower COGS during inflation leads to higher net income, potentially boosting share prices and attracting investors. However, it may not reflect current inventory costs and can create deferred tax liabilities.

- WAC: Provides a smoother COGS flow, mitigating the immediate impact of inflation on financial statements. However, it may not accurately reflect current inventory values.

- Specific Identification: Offers precise cost tracking, crucial for high-value items in inflationary periods. However, it can be complex and time-consuming, especially for large inventories.

Example: Acme Electronics, facing inflation, chooses LIFO to reduce taxable income and attract investors. This boosts short-term financial performance but creates deferred tax liabilities that could impact future profitability.

Deflationary Environments:

- FIFO: Lower COGS during deflation leads to higher net income, potentially overstating profitability. However, it may not reflect the current market value of inventory.

- LIFO: Higher COGS during deflation reduces net income, potentially impacting investor confidence. However, it provides a more realistic representation of inventory value.

- WAC: Offers a smoother COGS flow, minimizing the immediate impact of deflation on financial statements. However, it may mask declining inventory values.

- Specific Identification: Allows for adjusting individual item costs to reflect deflation, ensuring accurate valuation. However, it can be resource-intensive in a large inventory setup.

Example: XYZ Retail, experiencing deflation, opts for WAC to maintain stable financial performance. This avoids immediate financial strain but may mask falling inventory values, leading to poor pricing decisions in the long run.

Navigating Complex Accounting Standards:

Accounting standards like International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP) dictate acceptable inventory valuation methods for different contexts. Understanding these regulations is crucial for ensuring compliance and avoiding penalties.

- Consulting with accounting professionals: Expertise can help companies navigate complex standards and choose the most appropriate method for their specific circumstances.

- Staying updated on regulatory changes: Keeping abreast of evolving accounting rules ensures compliant and accurate financial reporting.

- Documenting valuation choices: Clear documentation of chosen methods and justifications protects companies from potential audits or inquiries.

Selecting the optimal inventory valuation method is not a one-time decision. By understanding the advantages and disadvantages of each method in various economic climates, observing real-world examples, and navigating complex accounting standards, businesses can make informed choices that optimize financial performance, mitigate risks, and ensure compliance. Remember, the ideal method is the one that aligns with your specific industry, financial goals, and long-term vision, paving the way for sustainable success in any economic climate.

Choosing the Right Inventory Valuation Method for Your Business:

With various inventory valuation methods at your disposal, selecting the “right” one can feel like navigating a confusing maze. But fear not! By considering your specific circumstances, you can confidently choose the method that best illuminates your financial path. Here’s a roadmap to guide you:

Step 1: Know Your Industry:

- Dominant methods: Certain industries often have preferred methods (e.g., LIFO in manufacturing). Consult industry reports or peers for insights.

- Price trends: Are prices in your industry typically stable, volatile, or inflationary? This significantly impacts the suitability of different methods.

Step 2: Analyze Your Inventory:

- Composition: Do you deal with high-value, unique items (specific identification) or diverse, frequently purchased products (WAC)?

- Perishability: Are you managing perishable goods requiring FIFO to prioritize selling older items first?

Step 3: Consider Your Financial Goals:

- Transparency: Is clear and accurate financial reporting a top priority, favoring methods like FIFO or specific identification?

- Tax planning: Are potential tax savings during inflation critical, making LIFO an attractive option?

- Cost-efficiency: Do you prioritize simplified record-keeping and administrative efficiency, leaning towards WAC?

Step 4: Consult Your Accountant:

- Their expertise can help you interpret your industry norms, analyze your specific situation, and weigh the pros and cons of each method in detail.

- They can also discuss legal and regulatory requirements, like mandatory adoption of FIFO under IFRS in certain regions.

Remember:

- There’s no “one-size-fits-all” solution. The optimal method depends on your unique circumstances and priorities.

- Don’t be afraid to consider multiple methods and consult with your accountant to make an informed decision.

- Regularly review your chosen method as your business and industry evolve to ensure it still aligns with your needs.

By following these steps and seeking professional guidance, you can choose the inventory valuation method that not only illuminates your financial picture but also guides your business towards sustainable growth and success.

Real-World Examples of Inventory Valuation in Action:

Inventory valuation methods aren’t just theoretical concepts; they play a vital role in the everyday operations of businesses across industries. Let’s dive into some real-world examples to see how different companies choose their methods:

The Neighborhood Bakery:

- Method: FIFO

- Reason: Their bread and pastries have a short shelf life, making it crucial to sell older items first to minimize spoilage. Aligning with the physical flow of goods (oldest out first) and simplifying record-keeping makes FIFO ideal.

The Upscale Boutique:

- Method: Specific Identification

- Reason: Each designer dress or luxury watch carries a unique cost and value. Precise tracking individual items ensures accurate financial reporting, inventory management, and pricing strategies for high-value merchandise.

The Global Electronics Manufacturer:

- Method: LIFO

- Reason: They operate in an industry with volatile component prices. LIFO helps minimize tax burden during inflation by lowering reported profits based on more recent, higher purchase costs.

The Online Retailer:

- Method: WAC

- Method: They offer a vast variety of products with frequent price fluctuations. WAC simplifies record-keeping and provides a balanced cost representation for their diverse inventory, even if it comes at the expense of pinpoint accuracy for individual items.

The International Automotive Chain:

- Method: FIFO (in compliance with IFRS)

- Reason: Operating globally necessitates adherence to IFRS standards, which mandate the use of FIFO for inventory valuation. While other methods might offer specific benefits, compliance takes precedence.

Remember: These are just snapshots; the optimal method for each business depends on various factors. Analyzing industry norms, inventory composition, pricing trends, and strategic goals is crucial before making a decision. Consulting with an accountant can ensure you choose the method that best serves your specific needs and helps you achieve your financial objectives.

By understanding how real-world businesses select their inventory valuation methods, you gain valuable insights that can empower you to make informed decisions and optimize your own business’s financial performance.

Conclusion:

Inventory valuation is an important aspect of business accounting that allows businesses to accurately track the value of their inventory and calculate cost of goods sold. There are several methods available for inventory valuation, including FIFO, LIFO, WAC, and specific identification. Each method has its own advantages and disadvantages, and businesses should carefully consider their specific needs and accounting requirements when choosing a valuation method.

Take a Quiz Test - Test Your Skill

Test your inventory management knowledge. Short multiple-choice tests, you may evaluate your comprehension of Inventory Management.