Editorial Note: We are an inventory management software provider. While some of our blog posts may highlight features of our own product, we strive to provide unbiased and informative content that benefits all readers.

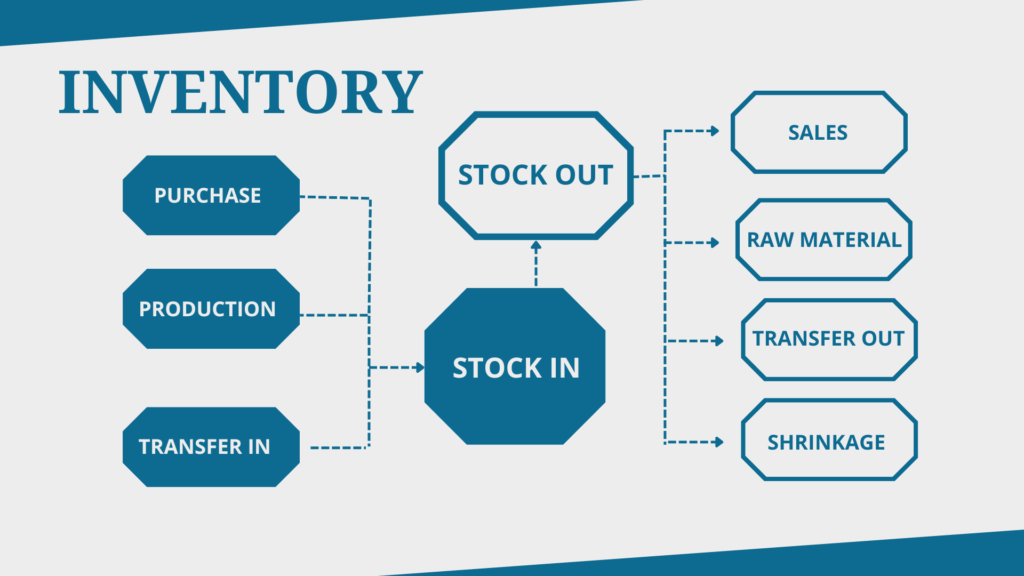

Inventory management is the process of overseeing and controlling the movement of goods in a company, from the time they are ordered to the time they are sold.

It involves managing the flow of products into and out of a company’s warehouse or storage facilities, ensuring that the right products are available in the right quantities at the right time.

The cost of inventory distortion in 2020 amounted to US$1.8trn[IHL Services]. It defines the importance of inventory management.

The goal of inventory management is to minimize the cost of inventory while ensuring that customer demand is met and that products are always available for sale.

Inventory management involves a number of key activities, including forecasting demand, monitoring stock levels, optimizing ordering and replenishment processes, setting safety stock levels, and reducing the cost of carrying inventory.

Effective inventory management is crucial for businesses because it helps minimize the risk of stockouts, reduce the cost of carrying inventory, and improve customer satisfaction by ensuring that products are always available.

Importance of Inventory Management for Businesses:

Inventory management is important for businesses because it helps them to effectively manage their inventory, which is one of their most valuable assets.

Here are some of the key reasons why inventory management is important:

1. Reduces the Cost of Inventory:

Effective inventory management helps businesses to minimize the cost of carrying inventory by reducing overstocking and obsolescence. By monitoring stock levels and ordering products only when needed, businesses can reduce the amount of money tied up in inventory.

2. Prevents Stockouts:

Inventory management helps businesses to avoid stockouts, which can lead to lost sales and dissatisfied customers. By monitoring stock levels and setting safety stock levels, businesses can ensure that products are always available for sale.

3. Improves Customer Satisfaction:

Effective inventory management helps businesses to improve customer satisfaction by ensuring that products are always available for sale. This can lead to increased sales and a more positive reputation for the business.

Inventory Management Operations:

Inventory management operations are the activities involved in managing a company’s inventory.

This includes the following:

- Demand forecasting: This is the process of predicting future demand for a company’s products. This information is used to determine how much inventory to order.

- Inventory planning: This is the process of determining the right level of inventory to have on hand. This is based on factors such as demand, lead time, and carrying costs.

- Inventory control: This is the process of ensuring that the company has the right amount of inventory on hand at the right time. This includes activities such as ordering, receiving, storing, and issuing inventory.

- Inventory valuation: This is the process of determining the value of a company’s inventory. This is important for financial reporting and for making decisions about inventory levels.

Effective inventory management is essential for businesses of all sizes. By managing inventory effectively, businesses can reduce costs, improve customer service, and increase profits.

Let’s See Inventory Operations With Cash Flow Inventory:

Cash Flow Inventory is a software solution designed to help businesses optimize their inventory management and improve inventory operations.

Here’s a breakdown of how Cash Flow Inventory can help with different aspects of inventory management:

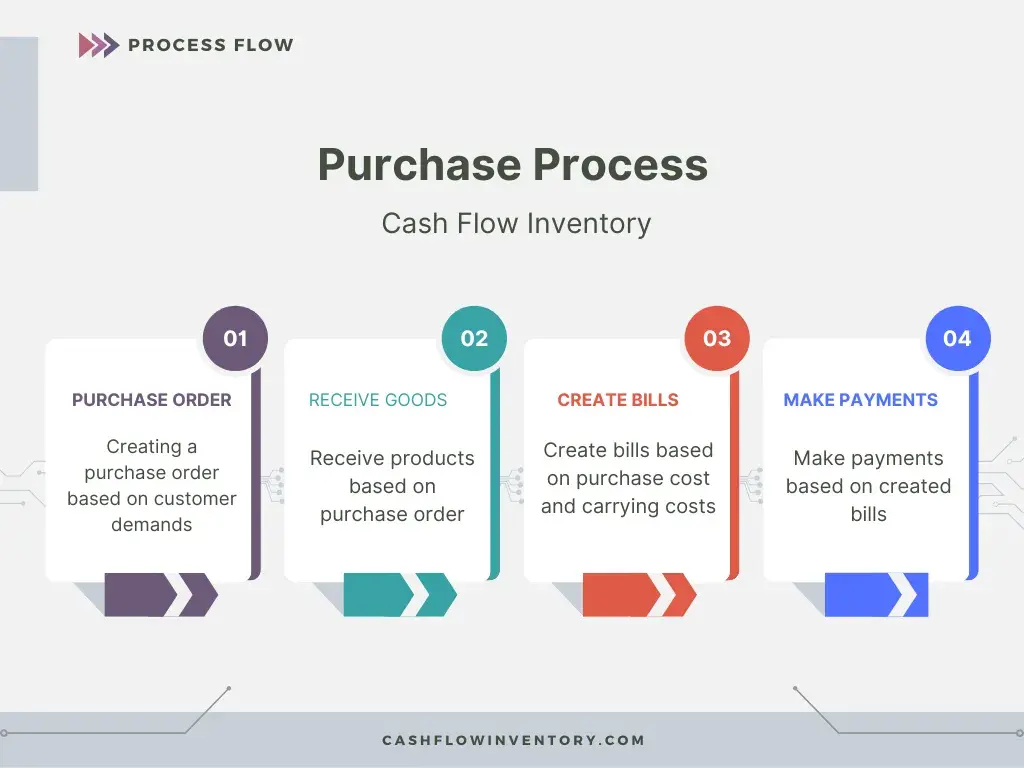

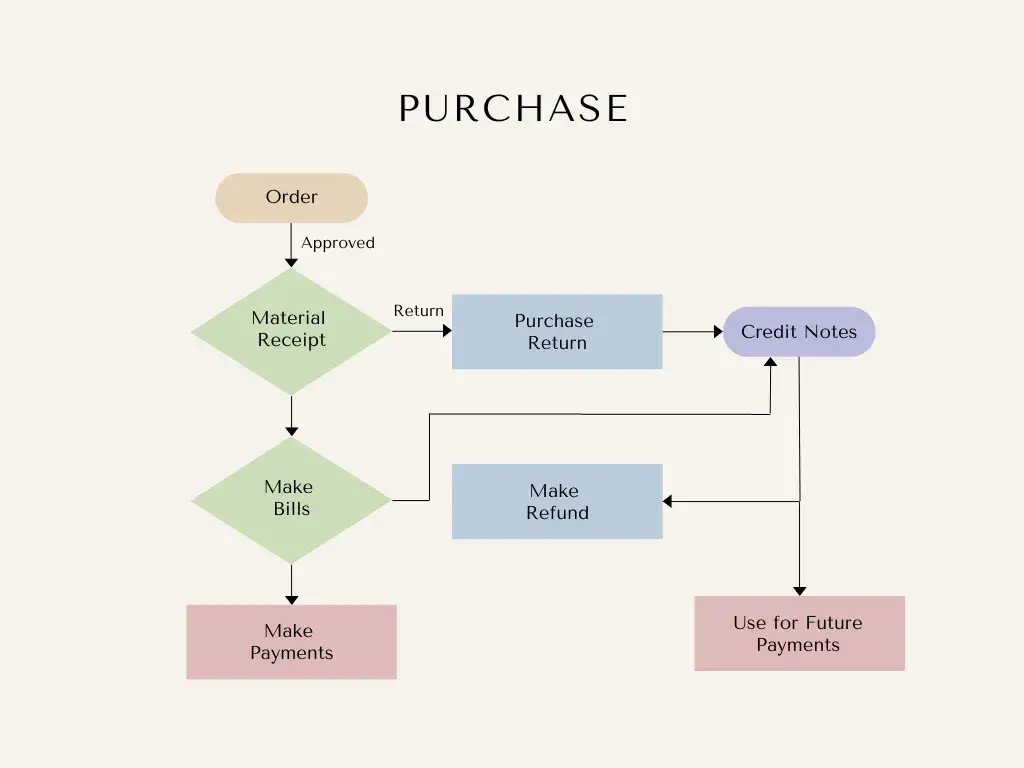

Purchasing Management:

The purchase part of the process involves the acquisition of goods or services from a vendor. It typically includes several steps, such as:

1. Purchase Order (PO) :

Once the purchase request has been approved, a purchase order is created in the organization’s procurement system. This document is sent to the vendor, outlining the details of the order, including quantity, price, delivery address, and payment terms.

The purchase order then goes through an approval process, where it is reviewed and approved by authorized personnel. The approval process may involve multiple levels of review, depending on the organization’s policies and procedures.

2. Receipt of Goods:

When the goods or services are received, the organization must confirm that the received goods match the PO. A receiving report is generated, and it is matched against the PO to verify that the goods have been received as expected.

3. Bill Creation:

Upon the receipt of goods, the vendor sends an invoice to the organization. The invoice should match the details on the PO, including the price and quantity of the items received.

4. Payment Processing:

Once the invoice is received, the organization reviews the invoice to ensure that it matches the purchase order and receiving report. The invoice is then sent for approval and payment processing.

Upon approval, the payment is processed, and the vendor is paid for the goods or services. Payment processing can be done via several methods, including check, electronic transfer, or credit card.

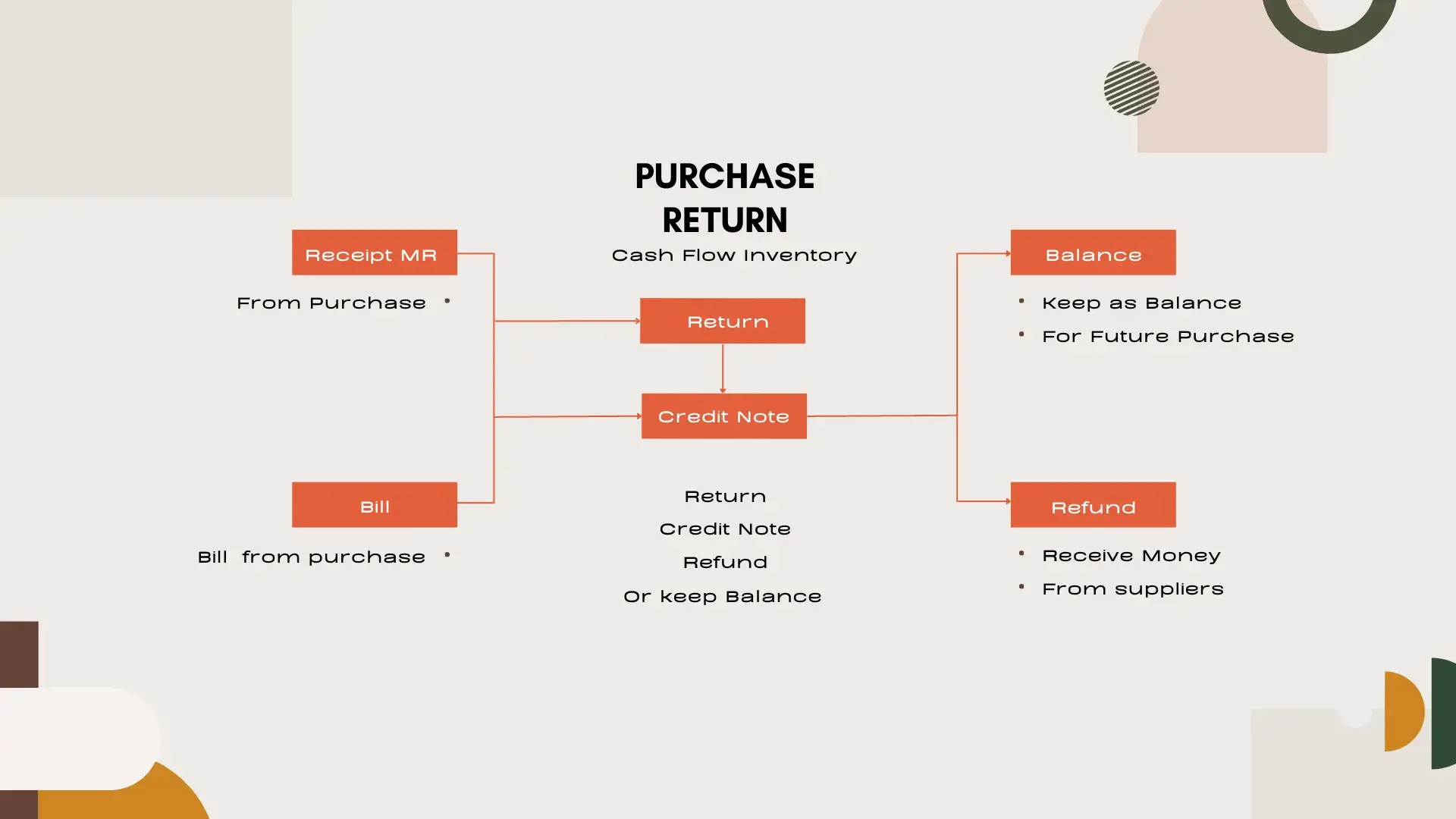

Purchase Returns:

The returns part of the process involves the return of goods or services to the vendor. This could be due to several reasons, such as:

1. Return:

The buyer contacts the vendor and requests a return, providing details such as the reason for the return and the original purchase order number.

The vendor reviews the request and may ask for additional details or evidence to verify the issue. If approved, the vendor authorizes the return and provides instructions for the return shipment.

The buyer ships the products back to the vendor according to the provided instructions.

The vendor receives the returned products and verifies that they match the details of the return request. They also check for any damages or defects to assess the condition of the returned items.

2. Credit Note:

If the returned items are accepted, the vendor issues a credit note, which documents the return of the goods and adjusts the original invoice accordingly.

3. Refund Processing:

Based on the credit note, the vendor processes the refund, which could be in the form of a credit to the buyer’s account, a check, or an electronic transfer.

Finally, the buyer records the refund in their financial records.

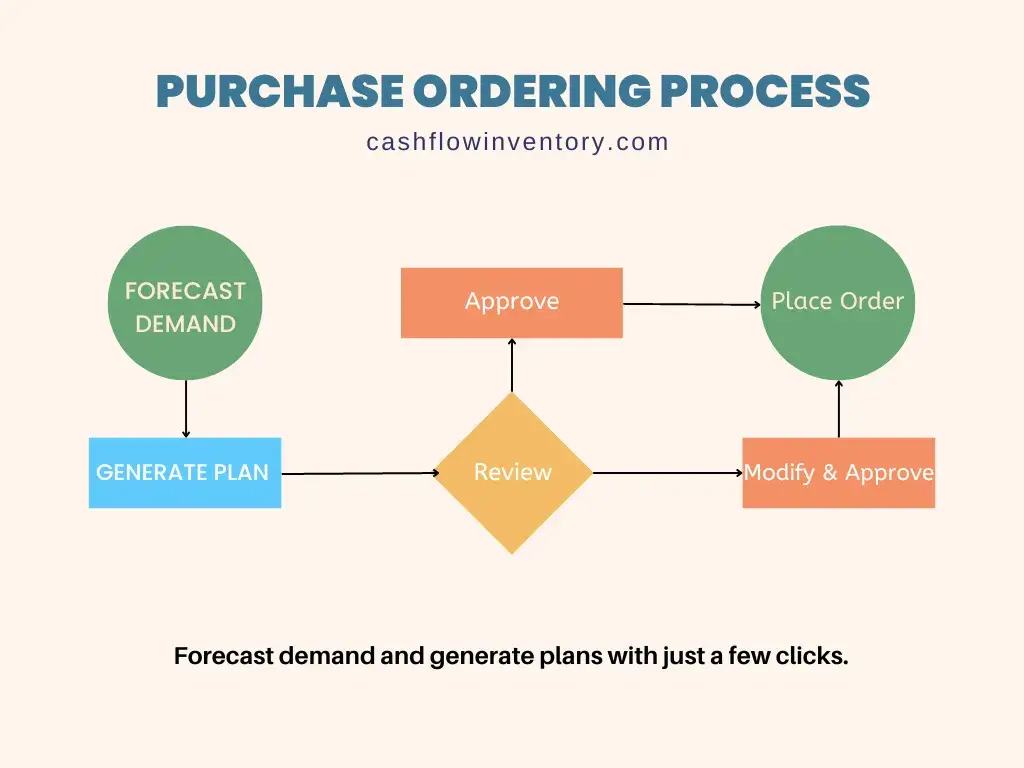

Purchase Planning & Placing Order with Cash Flow Inventory:

You can automate the process of forecasting demand and generating a purchase plan. The software also allows you to easily review and modify the purchase plan before placing a purchase order. Additionally, the software can help you manage the receipt of products and payments, ensuring that your purchasing process is efficient and effective.

1. Forecast Demand and Generate Purchase Plan:

The first step in purchasing management is to forecast demand and generate a purchase plan. To do this, go to the Purchase Plan section from software menu and enter the products that you want to purchase and the expected demand for each product. The software will then automatically generate a purchase plan based on this information.

2. Review and Modify Purchase Plan:

After the purchase plan has been generated, it will need to be reviewed by a purchase manager. The purchase manager can view the purchase plan and make any necessary modifications to the products or quantities before proceeding.

3. Place Purchase Order:

Once the purchase plan has been reviewed and approved, the purchase manager can place a purchase order. This can be done by going to the Purchase Orders section of the software and creating a new purchase order. Here, the purchase manager can select the products and quantities that are needed and enter any other relevant details.

Sales Management:

Cash Flow Inventory is an online inventory management software designed to help businesses manage their sales process effectively.

1. Sales order:

First of all, you need to create a sales order based on customers demand. This can be done by going to the Sales Orders section and clicking on the “New Sales Order” button. Here, you can enter the customer details, product information, and any other relevant details.

2. Product Issue:

Once the sales order has been created, you can issue the products from your store. This can be done by going to the Products Issuance section and selecting the sales order that needs to be fulfilled. You can issue products either partially or fully based on the order requirements.

3. Delivery Order:

Creation After the products have been issued, you can create a delivery order to ship the products to the customer. This can be done by going to the Delivery Orders section and selecting the sales order that needs to be fulfilled. Here, you can enter the delivery details, such as the shipping address and delivery date.

4. Invoice Creation:

Once the delivery has been made, you can create an invoice based on the delivery receipt. This can be done by going to the Invoices section and selecting the delivery receipt that needs to be invoiced. You can then enter the payment details, such as the payment method and due date.

5. Payments Receive:

Finally, you can manage your payments by going to the Payments section. Here, you can view all the payments that have been made and manage any outstanding payments.

Cash Flow Inventory is a powerful sales management tool that can help streamline your sales process and improve your cash flow. By following these simple steps, you can easily manage your sales orders, product issuances, delivery orders, invoices, and payments all in one place.

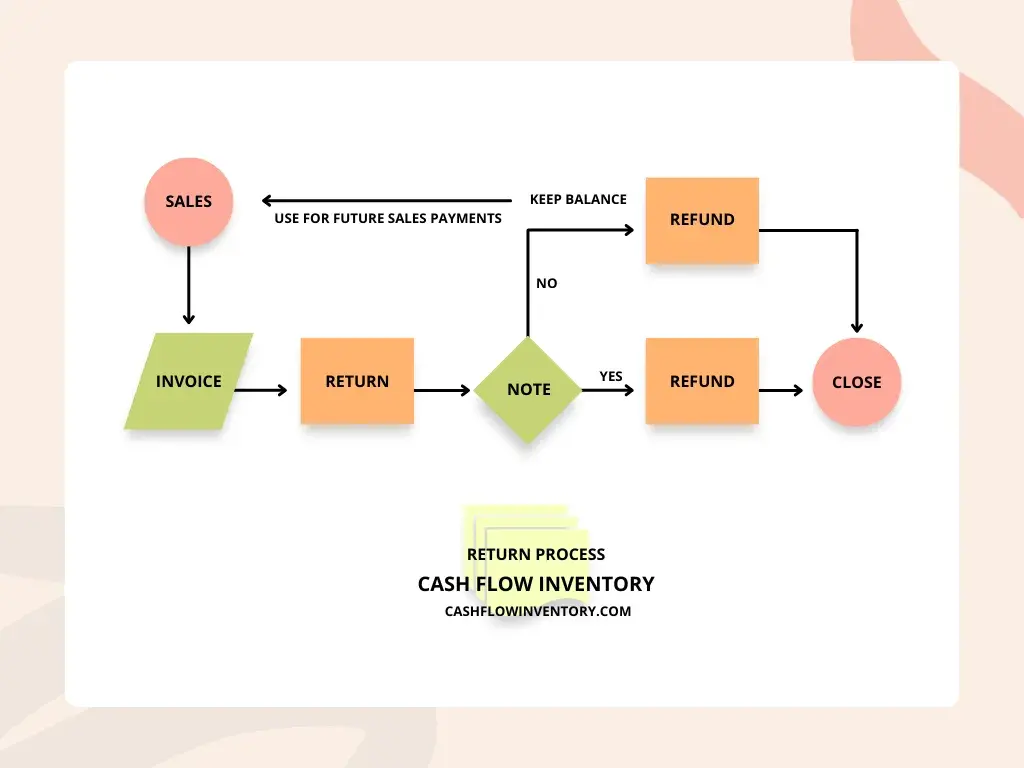

Sales Returns:

Sales returns, which occur when customers return merchandise they’ve purchased, are a crucial aspect of inventory management. Managing returns effectively is necessary to maintain accurate inventory levels and customer satisfaction.

1. Create a Sales Return:

To initiate a sales return, go to the Sales Returns section of the software and click on the “New Sales Return” button. Here, you can select the sales invoice that you want to return the products for. You can also enter the reason for the return and the products that are being returned.

2. Make a Note:

After creating the sales return, you can make a note about the return in the customer’s account. This will allow you to keep track of the customer’s balance and any future purchases that they make.

3. Make a Refund or Keep the Balance in Customer’s Account:

Next, you can choose whether to make a refund or keep the balance in the customer’s account for future purchases. If you choose to make a refund, you can enter the refund details and process the payment. If you choose to keep the balance in the customer’s account, you can adjust their account balance accordingly.

Stock Transfers:

Stock transfers, also referred to as stock movements or warehouse transfers, are the physical movement of inventory between locations within a business. This can involve transferring items between warehouses, stores, production facilities, or any other locations where inventory is stored.

1. Transfer Order:

- Initiation: The process begins with the creation of a transfer order. This document specifies the details of the inventory being transferred, including:

- Source location: The warehouse or store from where the inventory is being moved.

- Destination location: The warehouse or store where the inventory is being shipped.

- Item details: A list of the items being transferred, including their quantities, descriptions, and any relevant identification information.

- Transfer date: The date on which the transfer is scheduled to occur.

- Approvals: Depending on the organization’s procedure, the transfer order might require approval from various departments, such as finance or logistics.

2. Issue from Store:

- Picking and packing: Once the transfer order is approved, the picking and packing process begins. This involves:

- Identifying the correct items in the source location.

- Picking the required quantities and ensuring accuracy.

- Packing the items securely for transport.

- Labeling the packages appropriately with the transfer order details.

- Inventory documentation: The inventory system is updated to reflect the transfer of items from the source location. This may involve creating a stock transfer document and adjusting inventory levels.

3. Deliver Order:

- Transportation: The packed items are transported to the destination location using an internal or external carrier. The mode of transport depends on the distance, volume, and urgency of the transfer.

- Documentation: Transportation documents are prepared and accompany the shipment. These documents provide information about the shipment details, such as the contents, weight, and shipping route.

4. Receive:

- Verification: Upon arrival at the destination, the items are inspected and verified against the transfer order and packing slips. This ensures that the correct items and quantities have been received and that they are in good condition.

- Inventory update: The inventory system at the destination location is updated to reflect the receipt of the transferred items. This involves adjusting inventory levels and creating a receiving document.

- Put-away: Finally, the received items are placed in their designated storage locations within the destination warehouse or store.

Reporting and Analytics:

Reporting and analytics are critical components of successful inventory management. By providing valuable insights into inventory levels, trends, and performance, they enable businesses to optimize their inventory strategy and achieve significant benefits.

Reporting and analytics play a crucial role in effective inventory management. By providing valuable insights into inventory levels, trends, and performance, they help businesses optimize their inventory strategy and achieve significant benefits. Here are some key reasons why reporting and analytics are essential for successful inventory management:

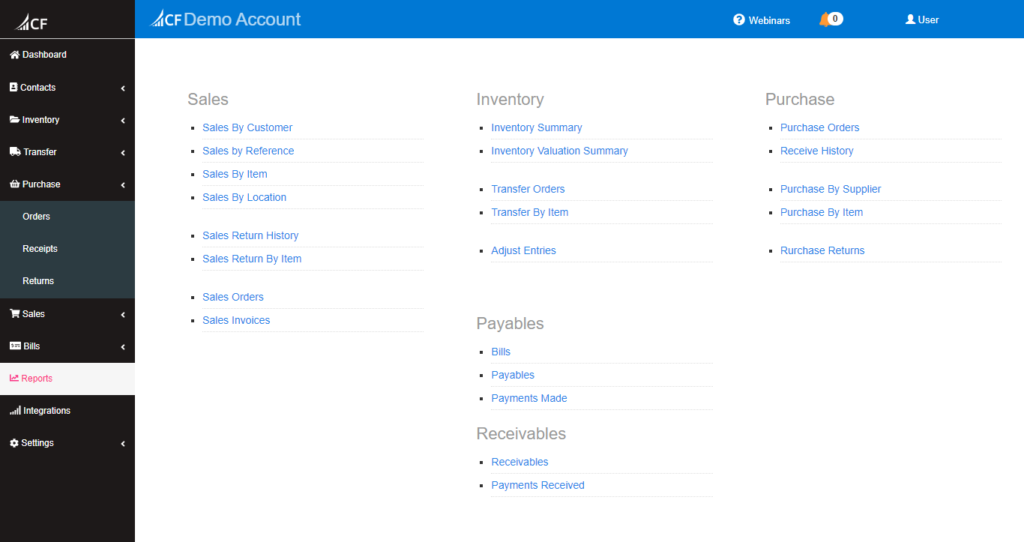

1. Sales Reports:

Sales reports are crucial documents that provide businesses with valuable insights into their sales performance, helping them identify trends, analyze strengths and weaknesses, and make informed decisions for future growth.

- Sales By Customer: This report shows the total sales made to each customer, allowing for analysis of customer profitability and sales trends.

- Sales by Reference: This report analyzes sales based on specific references, such as order numbers or promotions, providing insights into the effectiveness of different marketing campaigns.

- Sales By Item: This report breaks down sales by individual item, revealing which items are selling well and which ones need further promotion or inventory adjustments.

- Sales By Location: This report analyzes sales by location, helping to identify areas with strong sales potential and optimize resource allocation.

2. Sales Return Reports:

Sales return reports are crucial documents that provide businesses with valuable insights into returned goods and their impact on sales performance. By analyzing these reports, businesses can identify trends, understand customer behavior, and implement strategies to minimize returns and optimize sales.

- Sales Return History: This report tracks all sales returns over a defined period, providing insights into customer satisfaction and product quality.

- Sales Return By Item: This report identifies which items are most frequently returned, aiding in product improvement and inventory management.

3. Sales Order and Invoice Reports:

Both sales orders and invoices are vital documents in a company’s sales cycle. They provide a detailed record of customer orders and the associated financial transactions, enabling businesses to track sales performance, manage inventory levels, and ensure timely payments.

- Sales Orders: This report tracks open and closed sales orders, allowing for monitoring of sales pipelines and order fulfillment.

- Sales Invoices: This report provides a detailed breakdown of issued invoices, facilitating accurate cash flow forecasting and accounting.

4. Inventory Reports:

Inventory reports are crucial documents that provide businesses with a comprehensive overview of their stock levels, enabling them to manage inventory effectively, minimize costs, and optimize their supply chain. Let’s delve deeper into the different types and benefits of these reports:

- Inventory Summary: This report provides an overview of total inventory levels by category or location, helping to manage stock levels and prevent stockouts.

- Inventory Valuation Summary: This report analyzes the total value of inventory, assisting with financial reporting and cost analysis.

5. Transfer Order Reports:

Transfer order reports are essential tools for businesses managing inventory across multiple locations. They provide valuable insights into the movement of goods between warehouses, stores, or manufacturing facilities, ensuring efficient stock control and optimal supply chain management.

- Transfer Orders: This report tracks the movement of inventory between locations, enabling efficient stock management and analysis of inter-location inventory needs.

- Transfer By Item: This report analyzes the transfer of specific items, revealing trends and identifying potential inventory imbalances.

6. Adjust Entries Report:

Adjusting entries for inventory are crucial journal entries made at the end of an accounting period to ensure that the inventory value reported on the balance sheet accurately reflects the actual quantity and value of goods on hand. This report provides a detailed record of these adjustments, promoting transparency, auditability, and accurate financial reporting.

- Adjust Entries: This report tracks any adjustments made to inventory levels, providing transparency and auditability of inventory management practices.

7. Payables and Receivables Reports:

Payables and receivables reports are crucial documents for any business, providing valuable insights into the company’s financial health and operations. Let’s explore these reports in detail:

I. Payables:

These represent the amount of money a company owes to its suppliers, vendors, and creditors for goods or services received but not yet paid for.

- Bills: This report tracks outstanding bills to suppliers, supporting timely payment and accurate cash flow management.

- Payments Made: This report tracks payments made to suppliers, providing a record of payment history and facilitating supplier relationship management.

II. Receivables:

These represent the amount of money that customers owe a company for goods or services delivered but not yet paid for.

- Receivables: This report tracks outstanding invoices from customers, enabling efficient debt collection and improved cash flow.

- Payments Received: This report tracks payments received from customers, providing a record of payment history and supporting customer relationship management.

8. Purchase Reports:

Purchase reports are essential documents for businesses, providing valuable insights into their procurement activities and spending patterns. These reports empower businesses to optimize their purchasing processes, manage costs effectively, and make informed decisions regarding suppliers and resources.

- Purchase Orders: This report tracks open and closed purchase orders, allowing for monitoring of purchasing pipelines and inventory replenishment.

- Receive History: This report tracks the receipt of purchased goods, facilitating inventory management and ensuring timely updates to inventory records.

- Purchase By Supplier: This report analyzes purchases by supplier, helping to identify preferred suppliers and negotiate better pricing.

- Purchase By Item: This report tracks the purchase of specific items, revealing trends in purchasing behavior and supporting optimal inventory planning.

- Rurchase Returns: This report tracks the return of purchased goods, providing insights into supplier quality and facilitating efficient return processing.

These reports provide valuable insights into various aspects of your sales and inventory operations, enabling data-driven decision making and improved business performance.

Inventory Management Techniques:

There are a number of different inventory management techniques that businesses can use. The best technique for a particular business will depend on a number of factors, such as the type of business, the products that are sold, and the size of the business.

Some of the most common inventory management techniques include:

- Demand Forecasting: Predicting future demand accurately is crucial for effective inventory management. Various forecasting methods can be used, including historical data analysis, trend analysis, and machine learning. Choosing the most suitable method depends on your specific business and data availability.

- Just-in-time (JIT) inventory: JIT inventory is a system where inventory is only ordered when it is needed. This can help businesses to reduce costs by eliminating the need to carry excess inventory.

- Material requirements planning (MRP): MRP is a system that uses demand forecasts to determine the amount of raw materials and components that are needed to produce a product. This can help businesses to avoid stockouts and ensure that they have the right amount of inventory on hand to meet demand.

- Economic order quantity (EOQ): EOQ is a formula that can be used to determine the optimal order quantity for a product. This can help businesses to reduce costs by minimizing ordering costs and carrying costs.

- ABC Analysis: This technique categorizes inventory items based on their value and demand. A-items are high-value items with high demand, requiring close monitoring and tight control. B-items have moderate value and demand, warranting periodic review. C-items are low-value and low-demand items, requiring less control.

- Vendor-managed inventory (VMI): This allows your suppliers to manage your inventory levels, ensuring you have the right amount of stock on hand.

- Kanban systems: Kanban systems are a visual inventory management system that helps businesses maintain optimal stock levels while minimizing waste and improving efficiency. Developed by Toyota in the 1950s, Kanban is based on the Japanese word for “signboard” or “visual signal.”

- Dropshipping: This model allows you to sell products without holding any inventory. Orders are fulfilled directly by your supplier, reducing your storage and carrying costs.

The best way to learn more about inventory management is to speak with a qualified inventory management consultant. A consultant can help businesses to assess their current inventory management practices and develop a plan to improve their efficiency and effectiveness.

Challenges in Inventory Management:

Inventory management can present several challenges for businesses, including:

1. Managing Stockouts and Overstocking:

Maintaining the right balance between having enough inventory to meet demand and avoiding overstocking can be a challenge. Stockouts can result in lost sales and frustrated customers, while overstocking can tie up valuable capital and lead to obsolescence or spoilage.

2. Managing Obsolete or Slow-Moving Inventory:

Dealing with obsolete or slow-moving inventory can be a challenge for businesses, as it ties up valuable capital and may not provide a return on investment. Finding ways to dispose of or sell this inventory, such as through discount programs, liquidation sales, or other strategies, is important for effective inventory management.

3. Balancing Cost and Service:

Inventory management involves balancing the cost of holding inventory with the need to have inventory available to meet customer demand. Finding the right balance between these two factors can be difficult, as the cost of carrying inventory includes not only the cost of the inventory itself but also the cost of storing, insuring, and financing it.

4. Managing Complex Supply Chains:

As supply chains become more complex, managing inventory across multiple locations and suppliers can be challenging. This requires effective communication, coordination, and data sharing between all parties involved in the supply chain.

5. Adapting to Changes in Demand:

Rapid changes in demand can be difficult to manage, especially for businesses that hold large amounts of inventory. Quickly adjusting inventory levels in response to changes in demand can be challenging, especially for businesses that use traditional, slow-moving inventory management processes.

6. Dealing with Seasonality:

For businesses that sell products with significant seasonal fluctuations in demand, managing inventory levels can be a challenge. Accurately forecasting demand for these products, and adjusting inventory levels accordingly, is crucial to avoiding stockouts or overstocking.

7. Tracking and Managing Inventory:

Keeping accurate records of inventory levels and movements can be difficult, especially for businesses that have large amounts of inventory or complex supply chains. This requires effective tracking systems, strong data management practices, and regular audits to ensure that inventory records are accurate and up-to-date.

Industry-Specific Challenges:

While the core principles of inventory management remain constant, the practical application can vary dramatically across different industries. Each sector faces unique challenges based on product characteristics, demand patterns, and operational demands. Let’s explore how two common businesses – grocery stores and electronics retailers – navigate the inventory landscape:

Grocery Stores:

- Perishable Inventory: The constant threat of spoilage necessitates tight demand forecasting and efficient stock rotation. Frequent deliveries and smaller order quantities are crucial to minimize waste.

- Fluctuating Demand: Seasonal variations, promotions, and unpredictable weather patterns significantly impact demand predictability. Dynamic forecasting models and flexible purchasing strategies are essential.

- Space Constraints: With limited storage space, maximizing shelf utilization and optimizing product placement for faster picking become critical factors.

Electronics Retailers:

- High-value Products: Managing expensive inventory requires robust security measures and efficient warehousing practices to prevent theft and damage.

- Rapid Product Lifecycles: Technological advancements lead to quick product obsolescence. Accurate forecasting and just-in-time inventory management are key to prevent excess stock and lost profits.

- Seasonal Demand: Holiday seasons and new product launches trigger spikes in demand. Scalable inventory management systems and flexible supplier relationships are necessary to meet these surges.

By understanding these industry-specific challenges, businesses can tailor their inventory strategies for optimal efficiency and profitability. Implementing tools like ABC analysis and safety stock calculations can be further customized to address specific concerns, like prioritizing fast-moving items in grocery stores or minimizing obsolescence risk in electronics.

Remember, a one-size-fits-all approach to inventory management rarely succeeds. Recognizing the unique challenges within your industry empowers you to craft a targeted strategy that keeps your shelves stocked, your customers satisfied, and your cash flow healthy.

Inventory Management Best Practices:

Here are some of the best practices for inventory management:

- Use a cloud-based inventory management system: A cloud-based inventory management system can help you track your inventory levels in real time, set up reorder points, and generate reports.

- Keep accurate stock records: This is essential for ensuring that you have the right amount of inventory on hand at all times.

- Establish cost-efficient purchasing procedures: This includes negotiating with suppliers, setting up bulk discounts, and using just-in-time inventory management.

- Split inventory into different categories: This will help you to better track your inventory levels and identify items that are moving slowly or quickly.

- Develop active relationships with your suppliers: This will help you to ensure that you have a reliable source of inventory and that you are able to get the products you need when you need them.

- Set inventory goals: This will help you to focus your efforts on managing your inventory effectively.

- Monitor your inventory levels regularly: This will help you to identify potential problems early on and take corrective action before they become a major issue.

- Use inventory management software: Inventory management software can help you to automate many of the tasks involved in inventory management, freeing up your time to focus on other aspects of your business.

By following these best practices, you can improve your inventory management and achieve your business goals.

Here are some additional tips for effective inventory management:

- Use a barcode scanner or other inventory tracking system: This will help you to quickly and accurately count your inventory.

- Set up a system for tracking inventory movement: This will help you to identify items that are moving slowly or quickly and make adjustments to your inventory levels accordingly.

- Rotate your inventory regularly: This will help to ensure that your oldest inventory is sold first and that you are not left with outdated or obsolete products.

- Dispose of obsolete inventory promptly: This will help you to avoid carrying unnecessary costs.

- Train your employees on inventory management procedures: This will help to ensure that everyone in your organization is aware of their responsibilities and that inventory is managed consistently.

By following these tips, you can improve your inventory management and achieve your business goals.

Choosing the Right Inventory Management Tool:

Choosing the right software, however, can feel like navigating a jungle of options, each promising the inventory nirvana you crave. Cloud-based? On-premise? Feature-packed behemoth or nimble startup darling? Worry not, brave adventurer! This guide will be your machete, hacking through the undergrowth and revealing the perfect tool to tame your inventory beast and unleash your business’s true potential.

To simplify your search, let’s delve into key factors to consider:

Business Size and Needs:

- Small Businesses: Look for user-friendly, affordable solutions with core functionalities like purchase order management, basic inventory tracking, and reporting. Zoho Inventory and Sortly are popular choices.

- Mid-Sized Businesses: Prioritize scalability and integrations with existing systems. Consider options like Skubana by Extensiv or inFlow Inventory, offering multi-channel support and advanced forecasting tools.

- Enterprise-Level Businesses: Robustness, customization, and real-time data analytics are crucial. Explore comprehensive solutions like NetSuite or SAP Business One that integrate seamlessly with broader ERP systems.

Feature Focus:

- Warehouse Management: Prioritize features like barcode scanning, bin locations, and kitting functionalities if you manage a complex warehouse. Fishbowl Inventory or Katana MRP excel in this area.

- Ecommerce Integration: Seamless integration with your online store platforms like Shopify or Amazon is essential for multi-channel sellers. Ordoro and ShipBob excel in this domain.

- Manufacturing Focus: If you manufacture products, look for software with MRP (Material Requirements Planning) capabilities, like production scheduling and bill of materials management. Katana MRP and Prodsmart cater specifically to manufacturers.

Budget and Implementation:

- Cloud-based solutions offer flexibility and scalability at an affordable monthly cost, ideal for most businesses.

- On-premise software requires upfront investment and IT expertise but offers greater control and customization.

- Free trials and demos are available for most software, allowing you to test-drive features and assess user-friendliness before committing.

Remember, the “best” software is the one that seamlessly integrates with your existing workflow and addresses your specific pain points. Don’t hesitate to compare features, pricing, and user reviews before making your decision. By investing in the right inventory management software, you unlock a world of automation, accuracy, and valuable insights, propelling your business towards efficient inventory management and smoother operations.

Technologies Used in Inventory Management:

Several technologies are commonly used in inventory management to streamline operations, improve accuracy, and enhance efficiency.

Here are some key technologies used in inventory management:

- Barcode and RFID (Radio Frequency Identification): Barcoding and RFID technologies are widely employed for item identification and tracking. Barcodes are printed labels with unique codes that can be scanned using barcode scanners. RFID tags use radio frequency signals to transmit data, allowing for automated scanning without line-of-sight requirements. Both technologies enable quick and accurate inventory tracking and data capture.

- Inventory Management Software: Inventory management software provides a centralized system to track and manage inventory-related activities. It typically includes features like inventory tracking, demand forecasting, order management, reporting, and integration with other systems like point-of-sale (POS) or enterprise resource planning (ERP) systems. These software solutions help automate processes, provide real-time visibility, and optimize inventory levels.

- Warehouse Management Systems (WMS): WMS software is specifically designed to manage warehouse operations, including inventory control, order fulfillment, and labor management. It facilitates tasks such as inventory receiving, put-away, picking, packing, and shipping, improving warehouse efficiency and accuracy.

- Enterprise Resource Planning (ERP) Systems: ERP systems integrate various business functions, including inventory management, finance, sales, and purchasing. They provide a centralized database and streamline processes across departments, allowing for better inventory planning, coordination, and decision-making.

- Cloud Computing: Cloud-based inventory management systems offer several advantages, including accessibility from anywhere, scalability, and automatic software updates. Cloud solutions enable real-time data synchronization across multiple locations, facilitating collaboration and providing a flexible and cost-effective solution.

- Internet of Things (IoT): IoT technology connects physical objects to the internet, enabling data collection and communication. In inventory management, IoT devices such as sensors and smart shelves can monitor inventory levels, temperature, humidity, and other environmental conditions. This real-time data helps in demand forecasting, inventory optimization, and proactive maintenance.

- Mobile Devices and Mobile Apps: Mobile devices such as smartphones and tablets, coupled with inventory management apps, allow employees to perform various inventory-related tasks on the go. They can scan barcodes, update inventory records, receive alerts, and access real-time information, increasing efficiency and accuracy.

- Artificial Intelligence (AI) and Machine Learning (ML): AI and ML technologies can analyze vast amounts of inventory data, identify patterns, and generate insights for better decision-making. They can be used for demand forecasting, predictive analytics, optimizing reorder points, and identifying trends or anomalies in inventory patterns.

- Robotics and Automation: Warehouse automation technologies like automated conveyor systems, robotic arms, and automated guided vehicles (AGVs) streamline picking, packing, and material handling processes. These technologies reduce manual labor, improve efficiency, and minimize errors in inventory management.

These technologies, when implemented effectively, help organizations improve inventory accuracy, reduce stockouts, optimize inventory levels, streamline operations, and enhance overall supply chain performance. The choice of technology depends on the specific requirements, scale of operations, and budget of the organization.

Conclusion:

Inventory management plays a vital role in the success of any business. It involves monitoring and controlling the movement of goods and products, from procurement to delivery to customers. Effective inventory management helps businesses lower costs, boost efficiency, enhance customer satisfaction, and gain a competitive edge in the marketplace.

Related Post:

Demand Forecasting and Inventory Optimization | Proven Success

Unlock capitals from unnecessary inventory. Inventory optimization means keeping the proper levels of stocks according to demands where you can avoid empty stocks, overstocks, and dead stocks.

Read This Article

Take a Quiz Test - Test Your Skill

Test your inventory management knowledge. Short multiple-choice tests, you may evaluate your comprehension of Inventory Management.