Editorial Note: We are an inventory management software provider. While some of our blog posts may highlight features of our own product, we strive to provide unbiased and informative content that benefits all readers.

Excess inventory refers to any item a business has beyond its immediate needs. This can occur due to various reasons, such as overproduction, overstocking, poor demand forecasting, supply chain disruptions, and product obsolescence.

Excess inventory can have significant negative consequences for businesses, including increased costs, reduced cash flow, lost sales opportunities, decreased profitability, and damaged or obsolete goods.

While having some buffer stock is essential to handle unexpected demand, too much excess inventory can be detrimental to a business’s financial health.

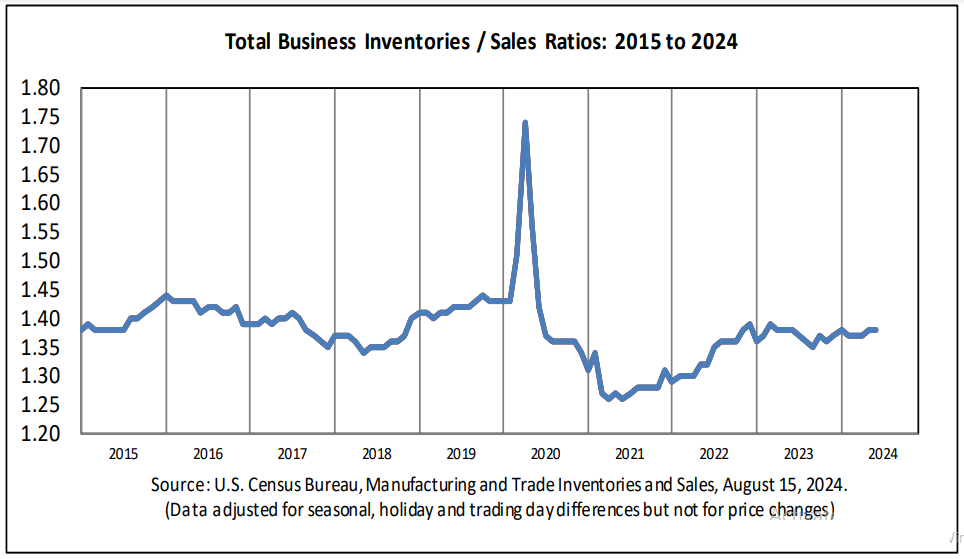

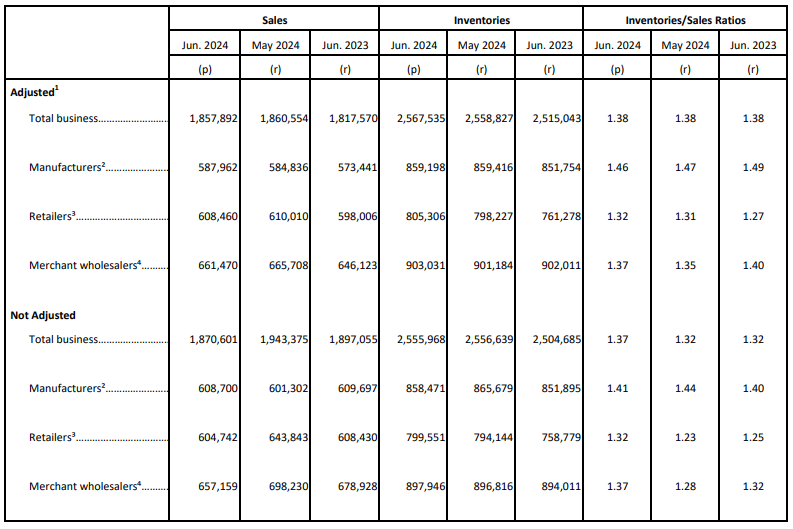

According to U.S. Census Bureau at the end of June 2024 :

Excess inventory can be a major headache for businesses of all sizes. It can tie up cash, take up valuable space, and lead to product spoilage. But with a little planning and creativity, businesses can turn their excess inventory into a profit generator.

Excess inventory can result in storage and management costs, potential product spoilage, and reduced profits. Companies must find ways to reduce or dispose of excess inventory to minimize its impact on their bottom line.

According to a new report by materials supplier Avery Dennison-

Despite efforts to sell excess goods to consumers, nearly 8% of surplus stock worldwide is ultimately wasted, resulting in $163 billion in lost inventory each year.

Importance of Addressing Excess Inventory:

Addressing excess inventory is crucial for the success of a business. By reducing excess inventory, businesses can improve their sales, reduce their holding costs, improve their lead times, reduce administrative costs, and free up capital for other growth initiatives. With the right approach and a commitment to addressing excess inventory, businesses can achieve their financial goals and position themselves for long-term success.

A study by the Journal of Business Logistics found that businesses that implement effective inventory management practices experience improved customer loyalty, with an average increase of 8%.

1. Reduced Costs:

Excess inventory takes up valuable storage space and incurs additional costs such as insurance, security, and handling fees. By addressing excess inventory, businesses can minimize these costs and free up valuable space.

2. Minimize Obsolescence:

Excess inventory can become obsolete if it is not sold within a certain timeframe, leading to losses for the business. By addressing excess inventory, businesses can minimize the risk of obsolescence and reduce the likelihood of holding onto inventory that becomes worthless.

3. Improved Supply Chain Management:

Addressing excess inventory can help businesses better understand their supply chain and identify areas for improvement. This can lead to more effective and efficient supply chain management, resulting in cost savings and improved customer satisfaction.

4. Better Inventory Turnover:

Effective inventory management and addressing excess inventory can lead to improved inventory turnover, which is a measure of a company’s efficiency in managing its inventory.

5. Improved Cash Flow:

Excess inventory ties up working capital and reduces the availability of funds for other important business expenses. By selling or disposing of excess inventory, businesses can improve their cash flow and have more funds available for other investments.

6. Increased Profitability:

By effectively managing inventory, businesses can reduce waste and increase profits. When excess inventory is sold or disposed of, it can generate additional revenue and improve the bottom line.

Different Types of Excess Inventory:

Understanding the different types of excess inventory is crucial for businesses to effectively combat this costly foe. By pinpointing the root causes of each category, targeted strategies can be implemented. From improved demand forecasting to optimized purchasing practices, the fight against excess inventory demands a multi-pronged approach.

- Obsolete inventory: This is inventory that is no longer in demand or has been replaced by newer products. Obsolete inventory can be caused by changes in consumer preferences, new technology, or the end of a product’s lifecycle.

- Dead stock: This is a type of obsolete inventory that has no chance of being sold. Dead stock can be caused by damage, poor quality, or a lack of demand.

- Slow-moving inventory: This is inventory that takes a long time to sell. Slow-moving inventory can tie up cash and lead to storage costs. It can be caused by poor sales forecasting, overstocking, or a lack of marketing.

- Excess seasonal inventory: This is inventory that is purchased for a specific season but does not sell out. This can be caused by inaccurate demand forecasting or changes in weather patterns.

- Damaged inventory: This is inventory that has been damaged during shipping, storage, or handling. Damaged inventory cannot be sold and must be either repaired, returned to the supplier, or disposed of.

The different types of excess inventory can have a significant impact on a business’s profitability. It is important to identify and address excess inventory early on to avoid these negative consequences.

Causes of Excess Inventory:

There are several causes of excess inventory, including overproduction, poor demand forecasting, slow moving product, unforeseen market changes, poor inventory management, and inefficient supply chain operations. By understanding the causes of excess inventory, businesses can take steps to mitigate its impact and improve their inventory management processes.

1. Overproduction:

Overproduction is a common cause of excess inventory, where businesses produce more product than what is actually needed. This can be due to a variety of reasons, such as incorrect demand forecasting, a desire to maximize production efficiency, or a lack of accurate information on inventory levels. Overproduction leads to an accumulation of inventory that is not sold and becomes excess inventory.

2. Poor Demand Forecasting:

Poor demand forecasting is another major cause of excess inventory. Businesses that do not accurately predict customer demand are at risk of producing or purchasing more product than they actually need, leading to an accumulation of excess inventory. This can be due to a lack of market research, outdated demand data, or the use of incorrect forecasting methods.

3. Slow Moving Product:

Product that does not sell quickly can become excess inventory over time. This can be due to a variety of reasons, such as product obsolescence, changes in consumer preferences, or overproduction of product. Businesses that do not regularly review their inventory levels and adjust production accordingly are at risk of having excess inventory.

4. Unforeseen Market Changes:

Unforeseen market changes, such as economic downturns, changes in consumer preferences, or new competition, can also lead to excess inventory. Businesses that are not able to adjust quickly to these changes may end up with excess inventory as demand for certain products decreases.

5. Poor Inventory Management:

Poor inventory management processes, such as failing to regularly review inventory levels or not accurately tracking inventory levels, can also lead to excess inventory. This can result in businesses having too much product in stock and not being able to sell it in a timely manner.

6. Inefficient Supply Chain Operations:

Inefficient supply chain operations, such as slow shipping times or product returns, can also contribute to excess inventory. Businesses that are not able to manage their supply chain operations effectively may end up with product that is not sold and becomes excess inventory.

7. Inaccurate Lead Time:

Another common cause of excess inventory is inaccurate lead time. Businesses that do not accurately estimate the time it takes for a product to be manufactured or delivered may end up with excess inventory. This can result in businesses having too much product in stock and not being able to sell it in a timely manner.

8. Low Product Quality:

Low product quality can also contribute to excess inventory. Products that do not meet customer expectations can become slow-moving and eventually become excess inventory. This can lead to a loss of revenue and harm the business’s reputation.

9. Disregard for Seasonal Trends:

Disregard for seasonal trends can also lead to excess inventory. Businesses that do not consider seasonal trends in their inventory management processes are at risk of producing or purchasing too much product during off-peak seasons, leading to an accumulation of excess inventory.

10. Unwillingness to Liquidate:

Finally, an unwillingness to liquidate excess inventory can also contribute to its accumulation. Businesses that are not willing to sell their excess inventory at discounted prices may end up with a large amount of unsold product that becomes a burden on their operations and finances.

Effects of Excess Inventory on a Business:

Excess inventory can have a significant impact on a business’s operations and finances. By addressing excess inventory, businesses can improve their inventory management processes, reduce costs, increase profits, and enhance their market competitiveness. Businesses must take a proactive approach to addressing excess inventory, considering factors such as inventory tracking, data management, communication, and market trends.

A study by the Journal of Supply Chain Management found that the cost of excess inventory can account for up to 10% of a company’s total revenue.

1. Financial Costs:

The accumulation of excess inventory can result in significant financial costs for a business. The costs associated with storing and maintaining excess inventory, such as rent, utilities, and insurance, can add up quickly and eat into the business’s profits. Additionally, the longer excess inventory sits in storage, the less valuable it becomes, leading to further financial losses.

2. Decreased Cash Flow:

Excess inventory can also decrease a business’s cash flow. Businesses that hold onto excess inventory are not able to convert that inventory into cash, which can strain the company’s financial resources and limit its ability to make investments or take advantage of business opportunities.

4. Wasted Resources:

Excess inventory can result in wasted resources. Businesses that hold onto excess inventory are using valuable resources, such as space, labor, and capital, to maintain products that are not being sold. This can result in a drain on the business’s resources and limit its ability to grow or expand.

5. Stock Obsolescence:

Excess inventory can also result in stock obsolescence, where products become outdated or irrelevant. This can lead to financial losses as the business must sell the products at a discounted price or dispose of them altogether.

6. Supply Chain Disruptions:

Excess inventory can also cause supply chain disruptions, as businesses may have to scramble to find storage space for the additional product. This can result in decreased efficiency and added costs, as well as delays in product delivery.

7. Decreased Product Quality:

Holding onto excess inventory for an extended period of time can also result in decreased product quality. The longer the product sits in storage, the more it may deteriorate, making it less valuable to customers.

8. Inefficient Use of Resources:

Excess inventory can also result in an inefficient use of resources. Businesses that hold onto excess inventory are not able to allocate those resources to other areas of the business, such as product development or marketing, resulting in a loss of competitiveness and missed opportunities.

How Do You Calculate Excess Inventory:

There are two main ways to calculate excess inventory:

- Basic Method: This involves comparing your current on-hand inventory to your expected demand. You can define expected demand in terms of a specific period, such as a month. Here’s the formula:

Excess Inventory = Current Quantity on Hand – Expected Demand (for a set period)

For example, if you have 500 units of a product in stock and your typical monthly sales are 100 units, your excess inventory would be 400 units (500 – 100).

- Inventory Turnover Ratio Method: This method provides a more nuanced view of excess inventory by considering how quickly your products are selling. A low inventory turnover ratio indicates you might hold on to stock for too long, potentially leading to excess inventory.

There’s no single formula for calculating excess inventory using the turnover ratio. However, a low ratio compared to historical data or industry benchmarks suggests potential excess inventory.

Here are some additional points to consider:

- Lead Time: When calculating expected demand, factor in the lead time it takes to receive new inventory. You wouldn’t want to run out of stock due to underestimating demand while waiting for a restock.

- Safety Stock: It’s wise to maintain a certain level of safety stock to buffer against unexpected demand fluctuations. This safety stock shouldn’t be counted as excess inventory.

Inventory management software can automate these calculations and provide valuable insights into your inventory health.

Strategies for Managing Excess Inventory:

Managing excess inventory requires a comprehensive and proactive approach. By implementing a combination of these strategies, businesses can improve inventory management processes, reduce costs, and increase profitability. Businesses must also be open to adapting and evolving their inventory management processes to ensure they remain effective in addressing excess inventory.

1. Regular Inventory Audits:

Conducting regular inventory audits can help businesses identify and address excess inventory. This can involve physically counting inventory, reviewing sales data, and examining inventory levels in comparison to demand.

2. Improved Inventory Tracking:

Improving inventory tracking processes can help businesses more accurately monitor inventory levels and prevent overstocking. This can include using inventory management software, automating inventory tracking processes, and implementing real-time tracking systems.

3. Reallocating Excess Inventory:

Reallocating excess inventory to different locations or product lines can help businesses avoid having too much inventory in one area. This can include transferring inventory to other stores, selling it through online marketplaces, or donating it to charitable organizations.

4. Adjusting Order Quantity:

Adjusting order quantities to better align with demand can help businesses avoid overstocking. This can involve reducing order sizes, increasing order frequency, or implementing a just-in-time inventory system.

5. Implementing Sales Promotion Strategies:

Implementing sales promotion strategies, such as discounts, promotions, and clearance sales, can help businesses sell excess inventory. This can also increase customer engagement and help businesses generate revenue from unsold products.

6. Evaluating Supplier Relationships:

Evaluating supplier relationships and negotiating better terms can help businesses avoid overstocking. This can include working with suppliers to establish better ordering processes, reducing order quantities, and improving communication.

7. Making Data-Driven Decisions:

Utilizing data-driven decision making can help businesses make informed decisions about inventory management. This can involve tracking sales data, analyzing customer behavior, and using predictive analytics to forecast demand. By making data-driven decisions, businesses can avoid overstocking and reduce excess inventory.

8. Conducting Market Research:

Conducting market research can help businesses better understand consumer demand and make informed decisions about inventory management. This can involve analyzing sales data, conducting customer surveys, and monitoring competitors to stay up-to-date on market trends.

9. Improving Lead Times:

Improving lead times can help businesses avoid overstocking by allowing them to better align inventory levels with demand. This can involve reducing lead times, implementing a just-in-time inventory system, or working with suppliers to improve delivery processes.

10. Diversifying Product Offerings:

Diversifying product offerings can help businesses avoid overstocking by reducing reliance on a limited number of products. This can involve expanding product lines, experimenting with new product categories, or exploring new market opportunities.

Selling Excess Inventory:

Selling excess inventory can be an effective way for businesses to reduce the costs associated with holding onto surplus stock and generate revenue. Here are a few strategies for selling excess inventory:

1. Liquidation Companies:

Partnering with liquidation companies can help businesses sell their excess inventory quickly and efficiently. Liquidation companies purchase surplus stock in bulk and sell it through various channels, such as online marketplaces and physical retail stores.

This approach can help businesses to reduce storage and handling costs, minimize the risk of obsolescence, and generate revenue from surplus stock. However, liquidation companies typically take a portion of the profits from the sale, so businesses need to be mindful of the costs involved.

2. Online Marketplaces:

Utilizing online marketplaces such as Amazon or eBay can be an effective way for businesses to reach a large, global audience and sell their excess inventory. Online marketplaces provide businesses with access to a vast customer base and a platform to sell products at a competitive price.

Additionally, businesses can use online marketplaces to test the market demand for their products before committing to a larger investment in production.

3. Wholesale Marketplaces:

Utilizing wholesale marketplaces can be an effective way for businesses to sell their excess inventory to other businesses and retailers. Wholesale marketplaces allow businesses to sell surplus stock in bulk at a discounted price, reaching a wide range of potential buyers.

This approach can help businesses to reduce storage and handling costs, minimize the risk of obsolescence, and generate revenue from surplus stock.

4. Auctions:

Holding an auction can be an effective way for businesses to sell their excess inventory to a large number of buyers. Auctions can be held online or in person, providing businesses with an opportunity to sell products to the highest bidder. This approach can help businesses to generate revenue from surplus stock and reduce storage and handling costs.

However, businesses need to be mindful of the costs associated with holding an auction, such as marketing, advertising, and handling fees.

5. Direct Sales:

Selling excess inventory directly to customers can be an effective way for businesses to generate revenue and reduce costs. This can involve holding sales events, offering promotions and discounts, or partnering with retailers to sell surplus stock. Direct sales can help businesses to reach a large number of potential buyers and generate revenue from surplus stock.

However, businesses need to be mindful of the costs associated with marketing and advertising their products, as well as the cost of storing and handling the surplus stock.

6. Trade Shows and Expos:

Participating in trade shows and expos can be an effective way for businesses to sell their excess inventory to a large number of potential buyers. Trade shows and expos allow businesses to showcase their products to a large audience and generate interest in their products. Additionally, businesses can use trade shows and expos to build relationships with other businesses, suppliers, and customers.

This approach can help businesses to generate revenue from surplus stock and reduce storage and handling costs. However, businesses need to be mindful of the costs associated with participating in trade shows and expos, such as booth fees, marketing, and advertising.

7. Employee Sales:

Utilizing employee sales can be an effective way for businesses to sell their excess inventory and reduce costs. This can involve offering employees the opportunity to purchase surplus stock at a discounted price. This approach can help businesses to generate revenue from surplus stock, reduce storage and handling costs, and engage employees in the sales process.

However, businesses need to be mindful of the legal and regulatory requirements involved in selling products to employees.

Strategies to Prevent Excess Inventory:

A study by the National Bureau of Economic Research found that businesses that effectively manage their inventory experience improved operational efficiency, with an average reduction in stock-outs of 20%.

Excess inventory lurks like a predator in the shadows of many businesses, waiting to pounce on unsuspecting victims. But fear not, intrepid warriors of commerce! With the right arsenal of strategies, you can prevent this profit-draining menace and keep your inventory lean and mean.

Here’s your battle plan:

Sharpen Your Forecasting Skills:

- Embrace data-driven insights: Utilize historical sales data, industry trends, and customer feedback to create accurate sales forecasts. Don’t rely on gut feeling – let the numbers guide you.

- Factor in seasonality and promotions: Don’t get caught off guard by seasonal fluctuations or special offers. Adjust your forecasts accordingly to avoid overstocking for predictable spikes or dips in demand.

- Stay agile and adaptable: The business landscape is dynamic, so be prepared to adjust your forecasts as needed. Regularly monitor market trends and customer sentiment to identify potential shifts in demand.

Master the Art of Procurement:

- Negotiate like a pro: Secure favorable pricing and contract terms with suppliers. Consider just-in-time inventory management, where you order products closer to the actual sales date, reducing carrying costs.

- Diversify your supplier base: Don’t rely on a single source. Having multiple suppliers mitigates risks associated with disruptions or price hikes from any one vendor.

- Implement minimum order quantities (MOQs) strategically: While larger orders often bring discounts, carefully evaluate your storage capacity and sales velocity before committing to bulk purchases.

Optimize Inventory Management:

- Conduct regular inventory audits: Physically verify your inventory levels regularly to identify discrepancies and prevent stockouts or overstocking.

- Embrace technology: Utilize inventory management software to track stock levels in real-time, automate reorder points, and gain valuable insights into product performance.

- Implement the ABC classification system: Classify your inventory based on value and sales velocity (A: high value/fast-moving, B: moderate, C: low). Focus on optimizing inventory management for A items, while considering alternative strategies like bulk discounts or extended lead times for C items.

Cultivate a Culture of Collaboration:

- Break down silos: Foster communication between sales, marketing, and procurement teams to ensure aligned forecasts and purchasing decisions.

- Incentivize smart inventory management: Implement performance metrics and reward systems that encourage employees to prioritize efficient inventory practices.

- Empower informed decision-making: Equip employees with the data and training they need to make informed choices about inventory levels and purchasing decisions.

Embrace Flexibility and Innovation:

- Consider consignment inventory: Partner with suppliers to stock products on consignment, minimizing upfront costs and risk associated with unsold items.

- Explore drop shipping options: Let suppliers handle storage and shipping, reducing your inventory burden and associated costs.

- Implement product lifecycle management: Proactively plan for product obsolescence by phasing out slow-moving items and introducing new offerings that align with current market trends.

By implementing these actionable strategies, you can transform your inventory management from a reactive struggle to a proactive dance, waltzing your way to increased profitability and a healthier bottom line. Remember, the key is to be mindful, data-driven, and adaptable. So, arm yourselves with these tactics, and go forth and conquer the beast of excess inventory!

Conclusion:

Excess inventory is a major challenge facing businesses today, and can have serious consequences for a company’s bottom line, efficiency, and productivity. From decreased sales and increased holding costs to increased lead times and administrative costs, businesses need to take steps to effectively manage their inventory in order to avoid these negative consequences.

Related Post:

Demand Forecasting and Inventory Optimization | Proven Success

Unlock capitals from unnecessary inventory. Inventory optimization means keeping the proper levels of stocks according to demands where you can avoid empty stocks, overstocks, and dead stocks.

Read This Article

Take a Quiz Test - Test Your Skill

Test your inventory management knowledge. Short multiple-choice tests, you may evaluate your comprehension of Inventory Management.