Editorial Note: We are an inventory management software provider. While some of our blog posts may highlight features of our own product, we strive to provide unbiased and informative content that benefits all readers.

Inventory costs are the expenses incurred in holding or storing goods for sale. It includes costs such as purchasing, storage, handling, insurance, and obsolescence. Companies strive to maintain a sufficient level of inventory to meet customer demand while keeping inventory costs low in order to increase profitability.

Inventory cost is one of the most important factors to consider when managing a business. The cost of inventory can have a major impact on a company’s bottom line and can be the difference between profit and loss.

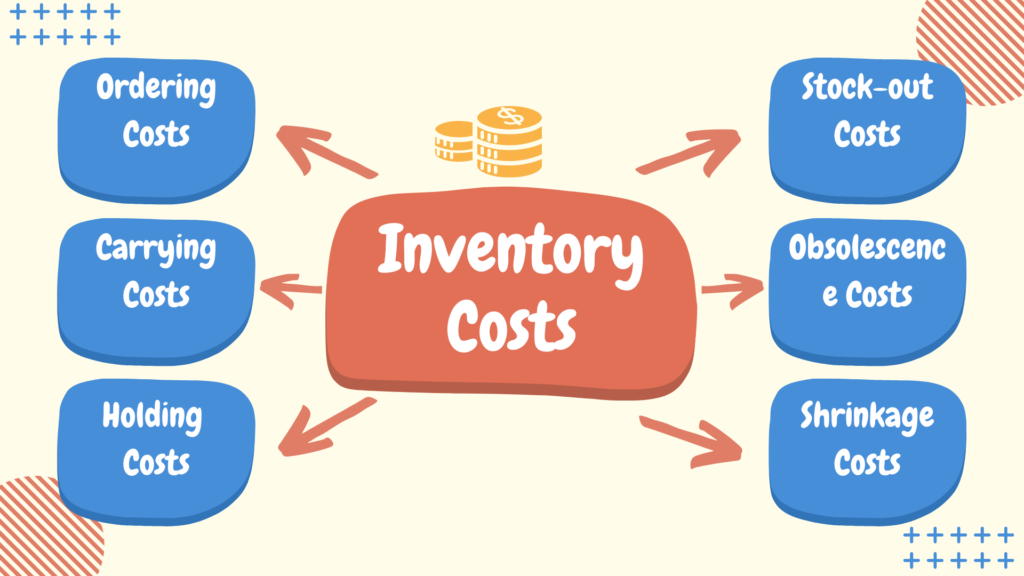

Types of Inventory Costs:

There are several types of inventory costs that businesses must take into account when managing their stock. These include:

1. Ordering Costs:

The costs associated with placing an order for new inventory, such as the cost of the goods themselves, shipping and handling, and any other related expenses.

Ordering costs are the costs associated with placing an order for inventory. These costs can include the cost of the inventory itself, the cost of shipping and handling, and the cost of any taxes or tariffs that may be associated with the order. Ordering costs can also include the cost of any storage or warehousing fees that may be incurred while the inventory is being held prior to shipment.

2. Carrying Costs:

The costs associated with storing and keeping inventory on hand, such as warehousing costs, insurance, and depreciation.

Carrying cost, also known as inventory holding cost, is the cost associated with storing inventory. This cost can include storage fees, insurance, opportunity cost, and shrinkage.

Carrying cost is an important factor to consider when managing inventory because it can have a significant impact on the bottom line. Too much inventory can tie up working capital and lead to higher carrying costs. On the other hand, too little inventory can lead to stock outs and lost sales.

The goal is to find the sweet spot that minimizes carrying costs while still meeting customer demand. This can be a challenge, but there are a few strategies that can help.

One way to reduce carrying costs is to implement just-in-time (JIT) inventory management. This is a system where inventory is only ordered and delivered as needed, which minimizes the amount of inventory on hand.

3. Holding Costs:

The concept of holding costs is important to understand when managing inventory. Holding costs are the costs associated with storing and maintaining inventory. These costs can include storage costs, insurance, taxes, and depreciation.

Inventory is an important part of any business, but it is also a cost. Too much inventory can tie up cash that could be used elsewhere, and it can also create storage and maintenance problems. Managing inventory so that it is at the right level is crucial to a company’s bottom line.

The goal is to have enough inventory on hand to meet customer demand, but not so much that it becomes a burden. That means that businesses need to strike a balance between customer service and holding costs.

There are a number of ways to reduce holding costs. One is to reduce the amount of inventory on hand. This can be done by increasing the frequency of deliveries from suppliers or by reducing the lead time for orders.

4. Stock-out Costs:

The costs associated with not having enough inventory on hand to meet customer demand, such as lost sales and lost opportunity costs.

Stock-outs can be frustrating and costly, but there are ways to minimize the cost of a stock-out and get your business back on track.

The first step is to understand the cost of a stock-out. There are direct and indirect costs associated with a stock-out. Direct costs include the cost of the item that is out of stock, the cost of shipping the replacement item, and the cost of lost sales. Indirect costs include the cost of lost productivity and the cost of lost customer goodwill.

Once you know the cost of a stock-out, you can take steps to minimize the cost. One way to do this is to have a good inventory management system in place. This will help you to keep track of your inventory levels and help you to avoid stock-outs.

5. Obsolescence Costs:

The costs associated with inventory that is no longer needed or used, such as the cost of disposal or the cost of storage for unused items.

Obsolescence costs are the costs associated with replacing or upgrading equipment, systems, or products that have reached the end of their useful life. These costs can include the cost of new equipment, installation, training, and disposal of the old equipment.

For businesses, obsolescence costs can be a significant expense, especially if they have to replace large pieces of equipment or systems. Obsolescence can also cause disruptions in business operations as new equipment is installed or employees are trained on how to use it.

There are a few ways to manage obsolescence costs. One is to plan for them in the budgeting process. This can help businesses avoid the financial shock of a large unexpected expense. Another way to manage obsolescence costs is to lease equipment instead of buying it. This can help businesses spread the cost of new equipment over time and avoid the need to dispose of old equipment.

6. Shrinkage Costs:

The costs associated with inventory that is damaged, destroyed, or stolen.

There’s no denying that shrinkage is a huge problem for retailers. In fact, it’s estimated that shrinkage costs the retail industry $100 billion annually. That’s a lot of money that could be going back into businesses and benefiting the economy as a whole.

There are a number of reasons why shrinkage occurs. One of the most common is theft by employees. This can happen when employees are dissatisfied with their wages or working conditions. They may feel that they’re not being paid enough for the work they do or that their job is not fulfilling. As a result, they may decide to steal from the company to make up for what they feel is missing.

Other causes of shrinkage include shoplifting, errors in inventory, and damage to products. Whatever the cause, shrinkage is a huge problem for retailers. It’s important to be aware of the causes of shrinkage and to take steps to prevent it.

Formula for Calculating Inventory Cost:

Inventory cost is the cost of goods that a company has in stock. It includes the cost of the materials, labor, and other expenses incurred in the production of the goods. The inventory cost formula is:

Inventory cost = (Materials cost + Labor cost + Other expenses) / Number of units in stock

The inventory cost formula is used to calculate the cost of goods that a company has in stock. This information is important for businesses to know so that they can price their goods appropriately and make informed decisions about inventory levels.

There are several factors that can affect the inventory cost of a company. The most important factor is the number of units in stock. The more units that a company has in stock, the higher the inventory cost will be. Other factors that can affect inventory cost include the cost of materials, labor, and other expenses incurred in the production of the goods.

Inventory Cost Methods:

There are a few different methods of calculating inventory cost, including last in, first out (LIFO) and first in, first out (FIFO). Each method can produce different results, so it’s important to understand how each one works before making decisions about inventory.

Inventory cost can have a big impact on a company’s financial statements. It’s important to track and manage inventory cost carefully to avoid overspending and to keep financial statements accurate.

1. First-in, first-out (FIFO) method:

There are a number of different inventory cost methods that can be used to value inventory, but the most common and simplest method is the first-in, first-out (FIFO) method.

Under the FIFO method, the cost of inventory is based on the order in which it is acquired. The first items that are acquired are assumed to be the first items that are sold, and the cost of those items is charged to expense as they are sold. The remaining inventory is then valued at the cost of the most recent purchase. This method is used because it is easy to track and it provides a consistent cost basis for inventory.

The main disadvantage of the FIFO method is that it does not necessarily reflect the true cost of the inventory that is on hand.

2. Last-in, first-out (FIFO) method:

If you use the inventory cost method LIFO, you are essentially valuing your inventory using the prices of the most recent goods you’ve purchased. That means that if prices have gone up, your inventory will be valued higher than if you had used another method.

There are a few advantages to using LIFO. First, it more accurately reflects the current value of your inventory. Second, it can help you manage your taxes, since you’ll generally be paying taxes on the most recent, and therefore most expensive, goods you’ve purchased.

There are a few potential drawbacks to using LIFO as well. First, it can create distortions in your financial statements if prices fluctuate a lot. Second, it can be difficult to change from another inventory cost method to LIFO, since it can have a big impact on your taxes.

3. Weighted average cost:

Weighted average cost is a method used to calculate the average cost of inventory items that have different costs. The weighted average cost is calculated by multiplying the number of units of each item by its cost, adding up these products, and dividing the total by the number of units in the inventory.

This average cost per unit is then used to value the inventory and to determine the cost of goods sold when items are sold. The weighted average cost method assumes that the units in the inventory are interchangeable and that the cost of the items being sold is the average cost of all the items in the inventory.

This method is useful in cases where there is frequent movement of inventory, as it provides a more accurate reflection of the cost of goods sold compared to using a specific identification method or the first-in, first-out (FIFO) method.

The formula for calculating weighted average cost is:

Weighted Average Cost = (Total Cost of Inventory) / (Total Number of Units in Inventory)

Where:

Total Cost of Inventory = Sum of the cost of each item in the inventory

Total Number of Units in Inventory = Sum of the number of units of each item in the inventory.

The weighted average cost can be calculated on a periodic basis (e.g., daily, weekly, monthly) to reflect changes in inventory levels and cost.

4. Specific identification:

Specific Identification is a method of determining the cost of inventory that assigns a specific cost to each unit of inventory based on its unique characteristics, such as serial number or production date. This method is used when the inventory items are unique or have different costs, and the cost per unit is easily traced.

In this method, the cost of each unit of inventory is tracked separately, and the cost of goods sold is determined based on the specific units that are sold. This method is useful in cases where the inventory items are unique, such as one-of-a-kind works of art, or where the cost per unit is easily traced, such as with serialized items.

The advantage of the specific identification method is that it provides a more accurate reflection of the cost of goods sold compared to other methods, such as weighted average or first-in, first-out (FIFO). However, it also requires more detailed record-keeping, which can be time-consuming and expensive.

5. Standard cost:

Standard cost is a method of determining the cost of inventory items by using predetermined costs for each item. The predetermined costs are based on factors such as labor and material costs, and are used to value the inventory and determine the cost of goods sold. The standard cost is established in advance, before the inventory is produced or acquired, and is used as a benchmark for measuring actual performance.

In the standard cost method, if the actual costs incurred during the production or acquisition of the inventory items are different from the predetermined standard costs, the difference is recorded as a variance. The variances are analyzed to determine the cause of the difference and to identify opportunities for improvement.

The advantage of the standard cost method is that it provides a benchmark for measuring actual performance and for identifying opportunities for improvement. This can be useful for companies that need to control costs, such as those operating in highly competitive industries.

The standard cost method also requires regular updates to the standard costs to reflect changes in production processes, materials, and other factors. Additionally, the method assumes that the standard costs accurately reflect the actual costs, which may not always be the case.

Factors Affecting Inventory Cost:

Inventory cost is the cost of buying, keeping and managing inventory. A variety of factors can influence it, including ordering or setup costs, carrying costs, stockout costs, purchasing costs, lead time, stock level, economic order quantity, product demand variability, and technological changes.

Inventory cost is affected by various factors, including:

- Production Volume: The amount of goods produced has an impact on the cost of inventory as production costs increase with larger volumes.

- Lead Time: The time taken from ordering raw materials to receiving them affects the cost of inventory as longer lead times result in increased storage costs.

- Order Quantity: The size of an order affects the cost of inventory as larger orders can lead to bulk discounts, but also result in increased storage costs.

- Carrying Cost: The cost of holding inventory includes expenses such as storage, insurance, and taxes. It increases with the amount of inventory held and the length of time it is held.

- Obsolescence Cost: The cost of inventory that is not sold or used is referred to as obsolescence cost, which increases as the length of time inventory is held increases.

- Market Demand: The demand for a product affects inventory costs as changes in demand can lead to overstocking or stock shortages, both of which can result in increased costs.

- Prices of Raw Materials: The cost of raw materials affects the cost of inventory as price changes can result in increased production costs.

By understanding these factors and considering them in inventory management, businesses can minimize the impact of inventory costs on their operations.

Importance of Inventory Cost:

Inventory cost is one of the most important factors that affect profitability. It is important to have a good understanding of the inventory cost in order to make sound financial decisions.

There are two types of inventory cost, direct and indirect. Direct inventory cost includes the cost of materials and labor used to produce the inventory. Indirect inventory cost includes the cost of storage, insurance, and taxes.

Inventory cost can have a significant impact on profitability. For example, if the inventory cost is too high, it may eat into the profits. On the other hand, if the inventory cost is too low, the company may not be able to meet customer demands.

It is important to strike a balance between the two in order to maximize profitability. A good way to do this is to track the inventory cost closely and make adjustments as needed.

Impact of Over Inventory Cost on a Business:

- Reduced profitability and competitiveness

- Tied up financial resources

- Decreased operating margins

- Lowered returns on investment

- Decreased company value

Impact of Low Inventory Cost on a Business:

- Improved financial performance

- Increased competitiveness

- Freed up financial resources

- Improved customer satisfaction

- Reduced stockouts.

Inventory Cost Management Best Practices:

There are a few different ways to reduce inventory cost. One way is to keep track of inventory levels and only order when necessary. This can be done by using a just-in-time (JIT) inventory system. Another way to reduce inventory cost is to negotiate with suppliers for better prices. This can be done by bulk ordering or by paying upfront for inventory.

Inventory cost can have a major impact on a business’s bottom line. It is important to carefully consider inventory cost when making decisions about inventory levels and ordering.

There are several strategies that businesses can use to manage inventory costs, including:

- Safety Stock Management: Safety stock is an extra amount of inventory held to ensure availability in case of unanticipated demand or supply chain disruptions. By managing safety stock levels effectively, businesses can reduce the cost of carrying excess inventory.

- Economic Order Quantity (EOQ) Model: This model calculates the optimal order quantity to minimize the total cost of ordering and carrying inventory.

- Forecasting and Planning: Accurate forecasting and planning can help businesses make informed decisions about inventory levels, reducing the risk of overstocking or stock shortages, and minimizing inventory carrying costs.

- Cost Reduction Initiatives: Cost reduction initiatives such as negotiating better terms with suppliers, reducing waste, and improving production processes can help lower the cost of inventory.

- Technology Adoption: The use of technology such as inventory management software and automated systems can help businesses monitor inventory levels, track costs, and make data-driven decisions about inventory management.

By implementing these strategies and continuously monitoring and adjusting inventory levels, businesses can effectively manage inventory costs and improve their overall financial performance.

How to Reduce Inventory Costs:

Inventory costs are a significant expense for many businesses, but there are a number of ways to reduce them.

By improving demand forecasting, reducing lead times, and using technology to track and analyze inventory, businesses can avoid overstocking, reduce obsolescence, and negotiate better prices with suppliers.

- Negotiate Better Terms with Suppliers: Negotiating better payment terms, discounts, or bulk pricing with suppliers can lower the cost of raw materials and production costs, reducing the overall cost of inventory.

- Optimize Order Quantities: Using the Economic Order Quantity (EOQ) model or other inventory optimization techniques can help businesses determine the optimal order quantities to minimize the total cost of ordering and carrying inventory.

- Improve Lead Time Management: Shortening lead times by collaborating with suppliers or using expedited shipping options can reduce the need for safety stock and minimize inventory carrying costs.

- Minimize Excess Inventory: By closely monitoring inventory levels and avoiding overstocking, businesses can reduce the cost of carrying excess inventory.

- Implement a Cycle Counting Program: Regular cycle counting can help businesses identify discrepancies in inventory levels, reduce the risk of stock shortages, and minimize obsolescence costs.

- Automate Inventory Management: Automated inventory management systems can help businesses monitor inventory levels, track costs, and make data-driven decisions about inventory management, reducing the risk of overstocking or stock shortages.

- Use Technology to Monitor Inventory Levels: The use of barcode scanning, RFID technology, or other inventory tracking methods can help businesses monitor inventory levels in real-time and make informed decisions about inventory management.

To be successful in reducing inventory costs, companies must continually monitor their inventory levels, review their inventory management processes, and be open to new strategies and technologies.

Conclusion:

Inventory costs are important for businesses to consider because they have a direct impact on a company’s financial performance. High inventory costs can erode profits, while a lack of inventory can result in stockouts and lost sales.

Effective inventory management helps companies to improve their cash flow, reduce the risk of stock obsolescence, and improve customer satisfaction by ensuring that products are available when they are needed.

In summary, managing inventory costs is essential for businesses to maintain profitability and competitiveness in their respective markets.

Related Post:

Safety Stock – Definition, Importance, Formulas & Implementation

There are a few different formulas that go into deciding how much safety stock you have to maintain. These include General formula,…

Read This Article

Take a Quiz Test - Test Your Skill

Test your inventory management knowledge. Short multiple-choice tests, you may evaluate your comprehension of Inventory Management.